The previous article on CBDC ended by saying that “a new mode of money is born, a new mechanism of payment & settlement is in progress and it is here to stay and transform international settlements.”

Let us see explore each of these statements & understand how it changes the status quo.

As we saw earlier in the series of articles, money is digital, sits in bank accounts, and any cross border payment utilises

(a) a network of trusted relationship between banks called the correspondent network (remember NOSTRO?) and

(b) requires the SWIFT network – a trusted messaging system, that is reliable & has widespread use.

Based on the instructions in the SWIFT messages, banks that service the NOSTRO accounts, transfer money and effect the international transfer. And banks as we know, will have to obey regulatory pressures like how US banks had to stop doing business with Russian entities. But if a bank or the banks in a particular country are banished from the SWIFT network, their international trade (and even national trade if that is how the country’s financial infrastructure is built on) can be crippled in one fell swoop.

Even otherwise, due to the multiple hops messages take through banks in different time zones, cross border payments are slow (takes about two days) and are costly, as each bank in the chain takes a cut.

This is where CBDCs change the game.

Several central banks have been working on a few important settlement mechanisms among themselves – directly & automatically instead of having to go through the SWIFT network. And since this CBDC network will be a multilateral arrangement, no country gets to monopolise it or have its finger on the kill switch.

A few proofs of concept have already been made.

-

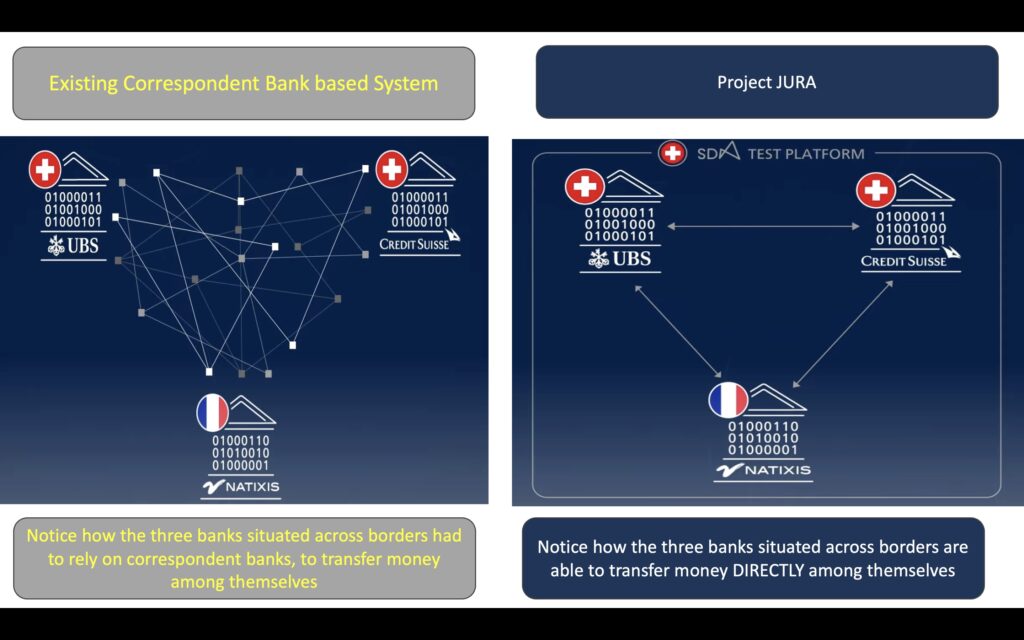

- Project Jura: This project explored the direct transfer of Euro and Swiss franc wholesale central bank digital currencies (wCBDCs) between French and Swiss commercial banks on a single blockchain platform operated by a third party. The multinational banks of Swiss & French origin – UBS, Credit Suisse & Natexis – performed a pilot with real value Foreign exchange transactions to validate technical feasibility. The result established the feasibility of DIRECT transfer of two currencies across banks instead of routing through correspondent banks and SWIFT network. The blockchain platform allowed both message and money to be transferred simultaneously. See below picture that makes it obvious.

-

- Project Dunbar: This project went a step further to understand the challenges that would be faced in settling multiple country issued CBDC transactions. It worked with CBDCs issued by the South African Reserve Bank, The Reserve Bank of Australia, Bank Negara Malaysia & the Monetory Authority of Singapore. The project was spearheaded by the innovation hub of the Bank for International Settlements (BIS). They worked with two technology parters (R3 & Partior – both working on blockchain platform in the finance space) in building two prototypes. The project showed the technical feasibility of the solution and identified bottlenecks in regulatory & governance issues across the jurisdictions of three countries and in how commercial banks within the country can access the multicountry platform.

BIS is the acronym for Bank for International Settlements headquartered in Basel, Switzerland. Established in 1930s and owned by 63 central banks from around the world, its mission is to support central banks’ pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks

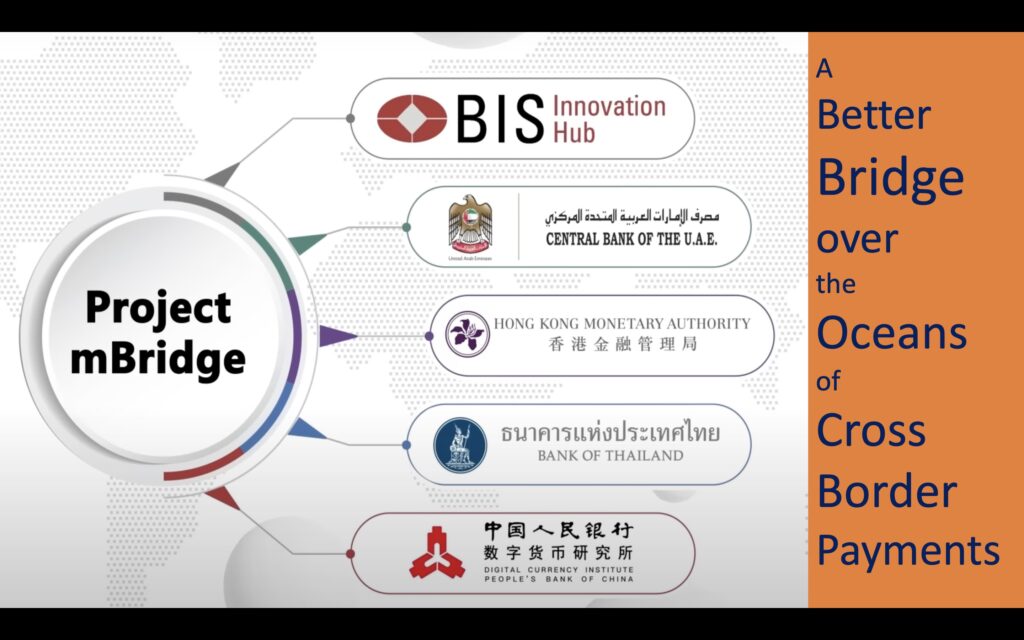

3. Project mBridge: Although now called mBridge, the project had metamorphasised from Inthanon to Project LionRock to mCBDC Bridge to the now popular mBridge platform.

This project too has been spearheaded by the BIS Innovation hub, but with four other central banks across the world. I will write a more detailed next article on mBridge so that we understand the details.

But first I want to make some common observations from the above projects.

-

- A realisation grew among all countries that cross border payments are too unwieldy, slow, costly and favours only those with (correspondent) “relationships” with other banks.

-

- There was disquiet among developing countries that the international payment system was controlled by a few countries in the world and a growing desire took root among them that this needed to change.

-

- So as part of the 2020 declaration, the G20 endorsed a roadmap prepared by the Financial Stabilty Board jointly with the Innovation Hub of the Bank for International Settlements in Switzerland. These projects we discussed above and a few more, are a consequence of this.

-

- Considering BIS being the guidepost of all Central Banks around the world, the initiatives taken up by BIS in this area have a greater chance of becoming reality.

-

- The new CBDC settlement mechanism across borders will help countries perform international trade in their own currencies instead of having to use a trade currency of a third country.

-

- This will further reduce the need for countries to stock up on huge reserves of the currently dominant trade currency(ies) (i.e. USD, EUR, etc) which makes them dependent on moving money through the banks of USA or Europe. This also makes the trading countries vulnerable to the rules of the third country. [Please recall the example of how a trade between Saudi Arabia and India had to comply with the rules of USA as explained in this article.]

-

- The new mechanism also reduces the huge dependence of countries on the SWIFT network over which the lifeblood trade & payment messages flow.

-

- In the previous article we saw how about a 100 countries are in various stages of implementing CBDC. This is a clear indication of the acceptance of these countries to the new mechanism and is a harbinger of the change in International trade settlements.

In the next article, we will see how mBridge system works and that gives us insights into the future of international cross border payments

[…] In, the shifting gears of cross border payments with CBDC, you will read about why several countries are implementing CBDCs and the different collaborative initiatives between countries in the world in this area. […]

What if there is a rogue entity in the network. In current mode, we have an intermediary that acts as custodian of data – absorbs intermediary risks

The network participants (banks) are pre-approved by the central banks of the respective countries. So, rogue element risk is not present. Reg. data custody, CBDC network works on blockchain with central banks / large banks as participants in the network. So it is not like a private blockchain where such risks are prominent.

[…] up on the previous article will give you a better context to understand this […]