Photo credit: Image by World Spectrum from Pixabay

The challengers and the challenges with them.

We know, that while Bitcoin will never gain currency as a currency (wouldn’t it be a crime to squander an opportunity at pun?), it showed how promising, the technology behind it is. Called ‘Blockchain”, its primary advantage in the financial payments industry is that it didnt need a clearing & settlement system for payments. Instead, it worked on a peer-to-peer direct settlement. In this aspect, it behaved like cash. Direct settlement between two parties without the need for an intermediary.

Keeping with the ethos of our blog, we will try to explain what type of a technology “Blockchain” is, to a lay audience with some common examples.

If you watch a sports match these days, say football or cricket, the scores of the teams are accounted for by a central unit. Irrespective of who all are behind it, lets keep the grand scoreboard in the stadium as the central unit. The scores are accounted for and published by the central unit and are final when it appears in the scoreboard. If we consider the teams to be two parties between whom the match is happening, the scoreboard is a third party. Any dispute in score will have to be taken up with them, because they are the gatekeepers…err, the scorekeepers – the central authorities!

Contrast this with how kids play the sport in local gullies. There is no central scoreboard, but each kid keeps the score in its head. Each goal or run will get accounted in each kid’s head and agreed upon commonly between them. If there is a dispute, they will go back to the previous point when all had agreed and will “re-build” the remaining score with all the events that had happened since that time. In a crude way, we can compare this to the distributed ledger technology of the Blockchain. Each node (kid) will keep count of the score and will proceed to the next step only if all nodes (kids) have reconciled with the score. Arguments like “is this a better system than centralised?” aside, there are business cases where this type of technology is useful. The crypto folks revel at the fact that there is no ‘all powerful’ central unit. So this is helpful to keep the gatekeepers (scoreboard) away. This egalitarian model is very appealing to the cryptocurrency worshippers and those who want to step away from central banks & governments.

Beyond the fact that there is no central unit, the fact that these records are ‘immutable” – -i.e. cannot be changed once registered- is very useful in maintaining non financial records also. Particularly when it comes to establishing provenance – like in maintaining transactions of land records, art collections etc. This technology has been used across the world from maintaining land records in Jamaica, to Toyota implementing this to maintain the provenance of the spare parts of its vehicles across all suppliers and its factories.

Beyond just being a “distributed ledger”, the technology can integrate with multiple third party applications to trigger events automatically. So when a Toyota supplier completes their supplies and the transaction is validated against the contract (the description, quality & quantity), their payments can be automatically made instead of someone having to verify the documents & initiate the payment. We saw how in international trade, banks play this role of verifying shipments against Letters of Credit. These can be automated using blockchain.

Several organisations across the world have come up with various uses with the Blockchain technology as its backbone.

So this is a pretty good technology with real life applications that is already in place over a wide variety of industries & geographies.

One of those applications is having “medium of exchange”. Several private companies came up with their own cryptocurrencies based on blockchain and paraded it as an asset whose value (ahem) will not erode like the value of fiat currencies (i.e. currencies issued by central banks) due to inflation. The thought is ambitious & lofty (in a sense that they will somehow circumvent the governments of the world) and they even made an argument that as an asset, it is superior.

If you have seen kids playing with Pokemon cards, they will also make a similar argument. Each card has a certain value, some more than the others and somehow each kid believes that it is sitting on a treasure trove because they have a stash of certain high value Pokemon cards. They will even name a price for each of them. Adults will be quick to realise that the value of these cards exists only in the minds’ of the kids but as far as they are concerned, these cards are just junk.

Truth be told, there are a lot of people who believe in the story of cryptocurrency & have exchanged real money (did you catch that I am implying crypto isnt?) for some fancy sounding cryptocurrencies. Some famous companies (like Tesla) even announced that they will sell their products in exchange for crypto, but rolled the decision back promptly in a few months. [Regular readers of this blog already know from this post, how a volatile currency poses problems in trade]. A country (El Salvador) even made Bitcoin a legal tender in the middle of 2021 and suffered a hit to its economy a year later.

A bigger truth be told, a currency is not just some technological tool that exists in vacuum. It is a deceptively simple looking instrument, which is backed by the strength of a country’s economy, managed through trade, economic, monetary, foreign policies and even more importantly by geo-politics. A single currency across borders will remain an utopian dream because all the policies (mentioned in the previous sentence) are governed within borders. Forget Bitcoin, if such a single currency across countries was even possible, the world would have had a single currency long back, making things simpler. Truth is, it is not simple. Even within Europe, that came together to have a common currency (Euro), some countries struggle because of the lack of flexibility this imposes on their monetary policy. Well-meaning & smart governments across the world will never cede their power to manage monetary policy to some faceless algorithm, however impressive it appears to be.

Ok lets get back to the challenger then. If such a currency is not possible, then what else will challenge the dominance of the USD?

To listen to an audio version of this article, please press the play button above.

————————————————————————————————————————————

Let’s start with answers to the questions posed in the previous article.

Q1: In this entire chain of cross-border payment transaction- where a company in India paid a company in Saudi Arabia, in which leg did the money actually move?

A: Money actually moved from one bank in the US to another in US. It did not cross any border!

But wasn’t this supposed to be a cross border payment? Money from India to Saudi?

Indeed! But because the payment was in USD, the transfer happened between two NOSTRO accounts in the US itself.

But what crossed borders, if money didn’t?

Messages! Yes just messages went beyond borders.

So if Adam Savage (of the popular TV show “Mythbusters”) were to investigate this, he would proudly proclaim – Busted!!

Contrary to popular perception in cross border payments, money doesn’t cross borders, only messages do.

But the companies in India and Saudi didn’t have USD accounts, they had INR and SAR accounts. Surely there must have been some conversion that must have happened?

Yes, that’s brings us to question no 2.

Q2: Where exactly did the currency conversion from INR to USD or USD to SAR happen?

In their respective countries.

INR- USD was done by SBI Mumbai and USD -SAR was done by AL Rajhi bank, Riyadh.

The banks in US don’t determine the exchange rate for any of the legs of this particular transaction.

Q3: Which countries’ compliances and regulations had to be applied in this transaction?

It is easy to guess that the compliance of governments in India and Saudi Arabia apply to these transaction as the buyer and seller are in these respective countries.

But here is the kicker. Just because the payment passes through banks in US, the compliance rules of the Govt. of the US of A also apply to this transaction.

If we zoom out of this single transaction and have a satellite’s eye view (a bird wouldn’t have so much of a span for our purposes), since most international trade happens in USD, ALL (yes all!) of those transactions have to comply with the rules of the Govt. of US of A.

-we can say that, just because USD is the world’s popular trade currency, central banks around the world buy and store it as a major reserve currency, thereby increasing the demand for USD perennially.

-the US govt is able to apply it’s writ on international transactions between two random foreign entities that are thousands of miles away from the shores of US, despite the fact the goods don’t come anywhere near the US.

Is this a good thing or a bad thing? Depends!

Depends on where you stand or how friendly one or both of the trading countries are with the US of A.

Let’s take just two examples to see the impact of this.

FATCA. Citizens of almost all countries around the world had to declare their FATCA status with banks around the world. Why? Because the US govt said unless each bank (called an FFI – Foreign Financial Institution) in every country collected and reported relevant data to the US on their FATCA status, US govt will withhold 30% of the value of bank’s qualifying (this is a subset of all txns) transactions going through US, done for FATCA non-compliant customers living in a foreign country. Considering almost all major banks around the world need to have USD NOSTRO accounts with banks in US, they have no choice but to comply.

FATCA (Foreign Asset Tax Compliance Act) is a US law since 2010 to track the income from the foreign assets of US citizens, living and maintaining accounts abroad. These assets could be Savings or fixed deposits in banks, Mutual Funds, Insurance products, real estate etc. As an example, if a US citizen has an account in Italy, the US govt wants to know. While most govts ask their citizens to declare their foreign assets and income voluntarily, the US govt goes one step further. It asks the banks’ and financial institutions of other countries to report, if any of the accounts they service for their customers, are for US citizens. To know this, the banks need to ask ‘every’ account holder to give a declaration of their US citizenship status.

With the US Dollar’s unique position of being an international trade currency, US was able to enforce compliance on every financial institution in 90 countries of the world, for an internal tax program. Who bears the operational costs and inconvenience of this compliance? – the respective banks. Who will the banks recover this cost from? Their respective customers. So here is an internal tax compliance program of the US govt, being paid for and complied with, by citizens of other countries around the world.

The second example is what happened as part of sanctions on Russia following the Ukraine-Russia war. US was able to successfully stall all (well, almost all) international trade if one of the trading partners was a Russian entity.

How is this even possible? Recall the organisation and messaging platform called SWIFT? And that it is owned by banks across Europe and US. (you can read more about SWIFT here). Also, if you recall the details of the SWIFT message in this article, you will know that every SWIFT payment message contains information on who originated the payment and who the beneficiary is. Combined with the fact that each USD transaction will have to go through banks in the US, it is easy for banks in the US to know who are the entities in an international transaction. As a result, the enforcement of this ban was quick, because US banks had a switch to identify and kill transactions, if one of the trading parties was Russian.

We need not get into the merits of the war or the sanctions. But if you look at it purely from a risk manager’s point of view, any country is at risk of immediate suspension of its international trade if they fall out of favour of the US. In that sense, the kill switch to the world’s international trade is in the hands of a few western nations.

Isn’t this a risk for other behemoths of international trade? like say – China? Yes and that’s why they try to wean away their international transactions from USD and are promoting Yuan based transactions. Or even trade based on bilateral currencies between China – Saudi Arabia, China- Iran, China- Russia (that’s no surprise). But it is not easy, because it is not just in the realm of economics or trade, but a matter of geo-political dominance. This game has had its players and many haven’t lived to tell their story.

There has been a recent challenger to this – albeit a tiny one- having some acceptance across countries, including the USA. You must have heard about Bitcoin and its cousins. These are & will be limited to miniscule, marginal, esoteric or arcane transactions and will not enter the mainstream as a force to reckon with.

But a bigger challenger is on the slow brew. The war that has already started in eastern Europe, and more wars that are about to start, are a reaction to it. Lets cover that in the next article.

Click on the urls below the images below to view the previous and next articles in this series

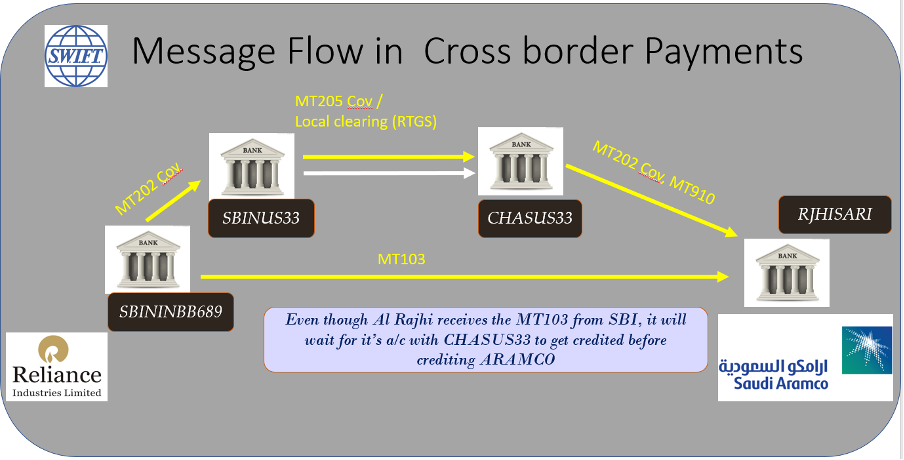

Let’s see at a high level how an international transaction happens. This time, we will use the most popular commodity transaction -oil — in our illustration.

The trade: In our example, the largest private sector refiner in India — Reliance Industries Ltd. (RIL hereafter) buys oil from Saudi Aramco of Saudi Arabia (we will refer to this as Aramco from here on). RIL banks with SBI, Fort branch, Mumbai and Aramco with Al Rajhi bank in Riyadh.

Most oil in the world gets sold in USD for the various reasons we saw in this article. Which means both buyer and seller will have to necessarily settle through a bank in US of A, irrespective of where they are. In our case, even though the seller is from Saudi Arabia and the buyer is from India, and the oil they exchange will never touch the shores of US of A, the commodity is priced in USD.

We can recall that the transaction will most likely be under the “letter of credit” and will involve the below parts.

LC Process: Before placing an order with Aramco, RIL will approach SBI to “Open” an LC favouring Aramco. Aramco will furnish it to its bank Al Rajhi and ask if the LC is trustworthy. If Al Rajhi is not comfortable with SBI’s trustworthiness or if their bilateral limits are exhausted, Al Rajhi can ask another bank to “confirm” SBI’s trustworthiness. By confirming this LC, this intermediate bank (say Citibank Riyadh) acts as a guarantor for SBI.

Since the transaction is to exchange Oil for Money, there are two Settlements. Since we have already seen the goods settlement in detail in the previous article (linked here), we will see how the money settlement happens in more detail here:

Goods settlement: When the ship calls on the port and unloads to the customs’ warehouse / oil farm, RIL, by sending an “acceptance” through SBI, gets the title for goods in the port / and lifts the goods. The payment terms can be on “Sighting” the goods — i.e pay the money and take the goods, or agree to pay x days after “accepting” to pay. The payment terms are as agreed upfront between the trade partners RIL & Aramco.

Money settlement: Since the transaction is in USD and as both SBI Mumbai and Al Rajhi, aren’t present in USD settlement zones, both of them need correspondent banks in the US of A to settle their transaction.

What are correspondent banks? These are banks where other banks maintain accounts — most often in a foreign country and in the currency of that country. So in our example, let’s say SBI Mumbai’s USD correspondent bank is SBI New York and Al Rajhi’s is JP Morgan Chase NY. By design these correspondent banks will be in US of A because that is where USD settlement happens. This correspondent relationship is not a transient one for ‘a’ particular transaction but are pre-established relationships between banks for long term. In fact, correspondent banks are listed publicly in a bank’s website and also figure in directories bankers use among themselves.

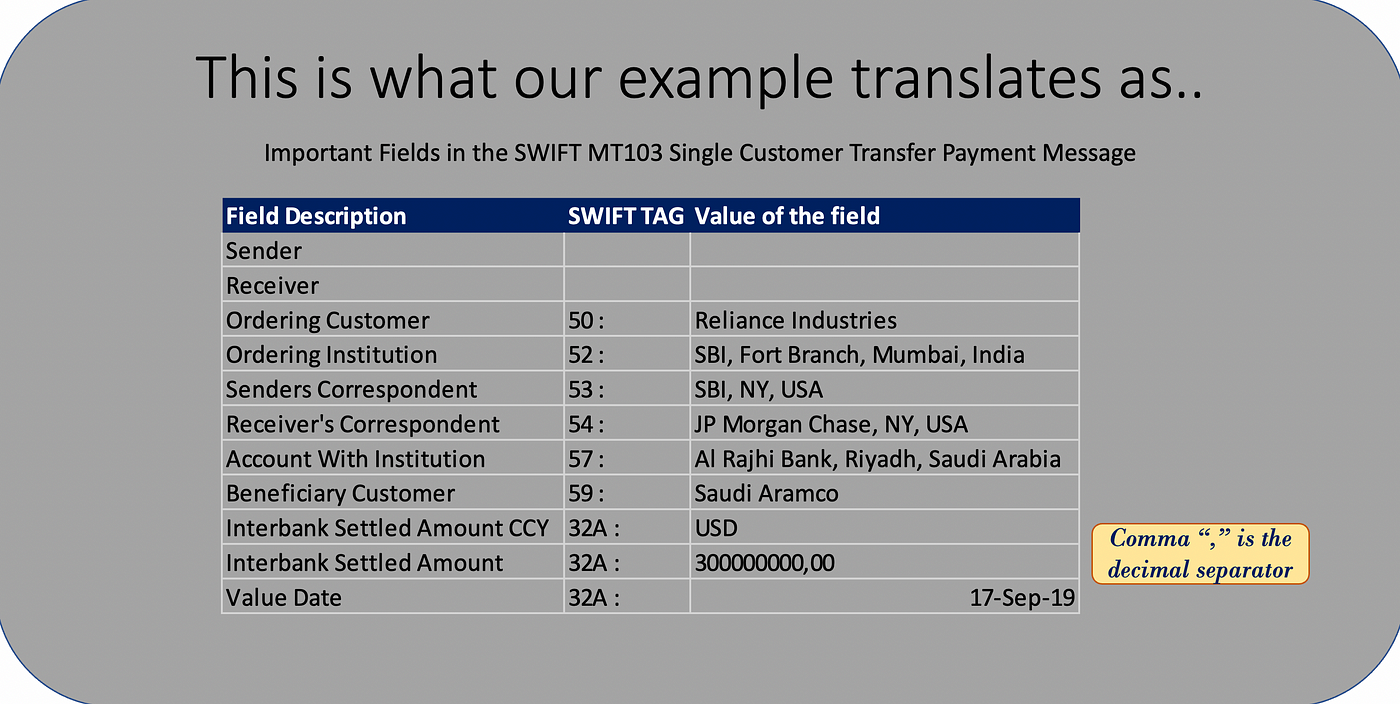

Now, back to our transaction. Here are the different parties in payment parlance. Note the banks are identified with their SWIFT BIC (Bank Identification Code, a unique code for each bank + branch combination, which will direct the SWIFT messages to them, like an email is sent to an email address) • Ordering Customer (the one who initiates the Payment): Reliance Industries • Ordering Institution (the bank that sets in motion the payment process within the banking system): SBI, Fort Branch, Mumbai SBININBB689 • Beneficiary of the Payment: Saudi Aramco, Saudi Arabia. • Account With Institution (the bank where the beneficiary holds an account): Al Rajhi Bank, Riyadh, RJHISARI • Sender’s Correspondent (the USD correspondent of the bank that sends the payment message): SBI New York, SBINUS33 • Receiver’s Correspondent (the USD correspondent of the bank that receives the payment message): JP Morgan Chase New York CHASUS33

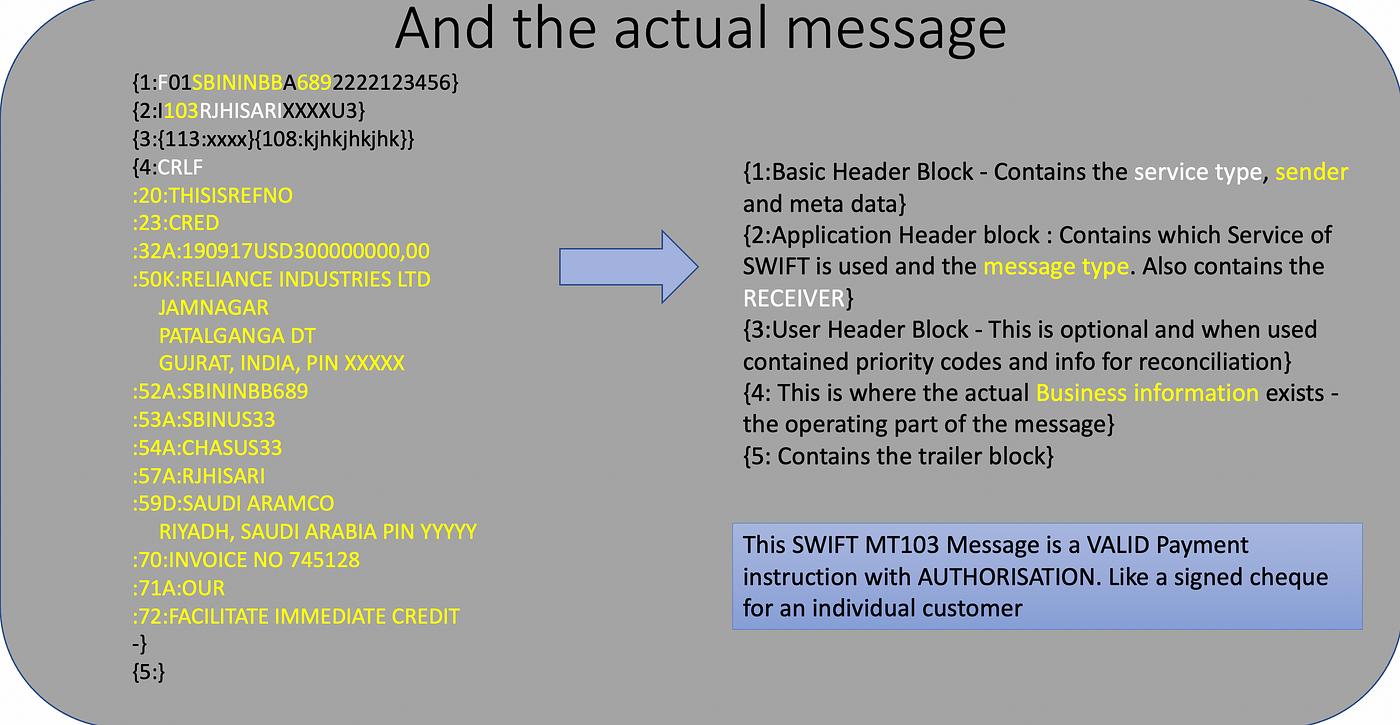

Each of these parties are identified in specific slots (called TAGs) in the respective SWIFT messages. For example the MT 103 message in our example will look like this.

When RIL asks SBI Mum to pay, say USD 300 Mn to Aramco’s a/c held with Al Rajhi, Riyadh, the payment will happen like this.

1. SBI Mum (SBININBB689) will send a (SWIFT MT103) message to Al Rajhi (RJHISARI) saying that it is arranging payment through

the mentioned correspondent banks and that is against specific invoice number 745128. This MT 103 is a “Customer payment message”. Which means there is a customer on behalf of whom the payment is initiated.

2. SBI Mum will “inform” SBI New York (SBINUS33) through SWIFT MT 202COV to pay Al Rajhi’s a/c with JP Morgan Chase New York, with specific account number details.

Couple of clarifications here:

How would SBI MUM know who is Al Rajhi’s USD correspondent or even the account number? Aramco would have shared this with RIL, which in-turn would relay it to SBI MUM. Even without Aramco telling them, the USD correspondent would be available in commercially available directories in the market that all banks subscribe to. These are like the yester-year telephone directories that give the different correspondent banks of most banks in the world in each currency.

What is this MT202COV? It is a message type to be used when a bank instructs its correspondent bank in a foreign country to move funds from its own account, to complete a customer payment it initiated. This type of payment mechanism is called the ‘Cover” method and hence the “COV” next to the message type MT202. Banks send similar messages to their correspondents for their own purposes as well. In such cases they will simply use the message type MT202. I elaborate this to highlight how robust the SWIFT system is, which covers different scenarios of business and in-turn promotes its wide-spread acceptance, automation and even standardisation. To this date, SWIFT is the de-facto platform for transactions among banks across borders.

3. With the above information, SBI NY will transfer the funds to JPMC in the local clearing in US — either CHIPS or FEDWIRE. To inform JPMC that this is an intermediate step in an international payment emanating from India and that both SBI NY and JPMC NY are just cogs in this wheel of international payment, SBI NY will relay the payment details through a SWIFT MT 205 COV message.

MT205 is similar to MT202 except that 205 is sent between banks when the currency of transfer is a local currency for both the banks. Since USD is the local currency in US where SBI NY and JPMC NY operate, MT205 is used.

Now we come to the last leg.

4. Once Al Rajhi sees a credit in its account with JPMC, meant for Aramco, they will pass on the credit to Aramco. Else they will wait for a confirmation message from JPMC. This can come as another set of SWIFT messages — MT 202 COV or a Credit advice (called an MT 910). Only after this we can say the transaction can be said to have been “settled” i.e the cross-border payment transaction is said to be complete!

The reason I explained the above in detail is to set you thinking. Let me leave you to ponder over the below questions.

In this entire chain of cross-border payment transaction- where a company in India paid a company in Saudi Arabia, in which leg did the money actually move?

Where exactly did the currency conversion from INR to USD or USD to SAR happen?

Which countries’ compliances and regulations had to be applied in this transaction?

Once you have had time to think and have some responses, I will cover the answers and the impact in the next article.

When we visit a store to buy a product, we ‘see’ the product, ask for a quote, if satisfied about the product and quote, we buy it (of course, we will haggle if possible – over the price). Once we pay, the transaction gets completed.

Here the quote, trade and payment transaction happen almost simultaneously. There is an element of trust which we don’t often realise. It is the trust that, we, as a consumer have, that the shopkeeper will allow us to take possession of the product upon payment. Similarly the shopkeeper trusts that the payment will be made when the product is handed over.

When we order an item online in an unfamiliar website, we don’t ‘see’ the product itself but only a representation of it on the website. Having made the payment, a question lingers in our minds: “will the product come through as promised”? Or will I receive a brick in the mail. To overcome this, we choose from a set of “risk mitigation” activities:

(a) order ‘Cash on Delivery’ — so that we don’t have to pay if the product is not delivered to our satisfaction. Or

(b) order from a renowned website (like Amazon) that ensures a return if the product was either not delivered or was not as listed.

In cash-on-delivery, there is absolutely no risk for the buyer, however the seller bears several risks. He wouldn’t know if the buyer would accept and pay for the product and still needs to pay for the transportation if the product is returned by the prospective buyer. While the seller may not lose the product itself, there is a transportation cost involved. If the product is a perishable item (like a block of cheese), the possibility that it can perish in the back and forth journey and lose its entire value is real.

What a reliable platform like amazon does is, it brings trust for both parties with its robust return policy and feedback mechanism on products and sellers. Both buyers and sellers recognise this value addition by Amazon (or a similar service) and make long distance trade possible and vibrant — whether we are conscious about it or not.

This element of ‘Trust’ becomes even more pronounced if the trade is international — where additional transit times and customs complications are usual. Yet billions of goods and services get sold and bought across the oceans. Is there an Amazon like entity that provides trust? Well, it is not one single entity a network of banks (yes banks!) that provide this trust.

Let’s take an example of a trade between two very reputed, financially rock-solid and ethical companies. I say this because none of these companies will wilfully cheat the other and pose a credit risk to the other.

Caterpillar USA, (the manufacturer of those monster trucks we all love) and Balkrishna Industries Ltd., (India’s largest manufacturer of off-highway-tyres) sign a deal where BKT is to supply its famed “Earthmax SR 47” tyres for one of CAT’s off-Highway trucks. BKT has its plant in the western Indian state of Gujrat and CAT needs those tyres in Illinois, US to be fitted into those (monster) trucks.

The journey of those tyres, even before they start their journey moving trucks on the road, is a long one — inside containers from BKT’s plants in Gujarat, India by road to one of the ports in Western India, then by sea to the eastern seaboard of US and then again by road to Illinois. CAT will pay BKT only if the tires (since they have reached American shores, lets use the American spelling) it receives are of the specification they asked for and if the tires reach them in good shape. The journey of the Earthmax tires can be interrupted in the sea by storms, sea pirates off the coast of Somalia or even delayed by a random ship that runs aground in the narrow straits of Suez canal. Bottomline, the tires may not arrive at the warehouse of CAT in time, despite the best intentions of BKT.

Or, in spite of supplying the right tires braving all the interruptions on the way, BKT may not receive payment for what it delivered to CAT because — ahem, a political sanction was put in place due to one of those unforeseen risks we are slowly getting used to in these uncertain times.

These are risks that both the companies face!

As commercial public limited companies that need to answer their shareholders, these companies will employ the best international trade practices to de-risk. Enter — banks & their “Letters of Credit”.

In its simplistic terms, a letter of credit is an assurance by a bank that it will make payment to an exporter, as long as the exporter supplies the goods according to the terms agreed between the exporter and importer, at the agreed place.

If BKT indeed made available to CAT the tyres of agreed quality & quantity at the agreed place and provides documentation proving that, CAT’s bank will pay BKT’s bank to be credited to BKT.

And if BKT isn’t able to do that, CAT is protected and no money is paid to BKT.

Voila! We now have a mechanism of instilling trust in a trade between two companies across the oceans. Actually, this mechanism has been in place for decades — even before Amazon came into the picture.

Thus banks provide a very important ingredient (apart from money of course) — the trust needed for international trade & transactions.

Photo Credits:

Picture collages made from pictures & photos thanks to:

Photos by krakenimages & Ian Taylor on Unsplash

Photos by Mediamodifier & Coker free vectors on Pixabay

Photo by energepic.com through pexels.com

logos of respective companies

Click on the urls below the images below to view the previous and next articles in this series

Now that we understand the need for trust and how “Letters of Credit” (we will call this LC from here on) bridge the trust deficit among (relatively) unknown trade partners, let’s get into the mechanism of how they work.

Let’s carry on with the previous example of our fictitious trade between Caterpillar & BKT tyres.

Once CAT and BKT find each other suitable (for the transaction that is 😁 ), they enter into a contract that will determine

– what type of tyres BKT is selling, its technical specifications

– the quantity

– price,

– what does that price include (just the products, or freight & insurance too)

– where will it be delivered (at CAT’s location or is it sufficient if BKT delivers it to someone outside its own factory)

– when the tyres will be shipped / delivered

– how will the trade be carried out (through LC)

– which banks will be involved and who pays the fees

– how many days does CAT get to make the payment once the invoice is served

– any inspections to be done by a third party at the port where the tyres will be offloaded?

– Anything else they both (CAT & BKT) agree on.

So, in a sense, each and every foreseeable part of the transaction will be committed in the contract — including unforeseeable “force majore” clauses.

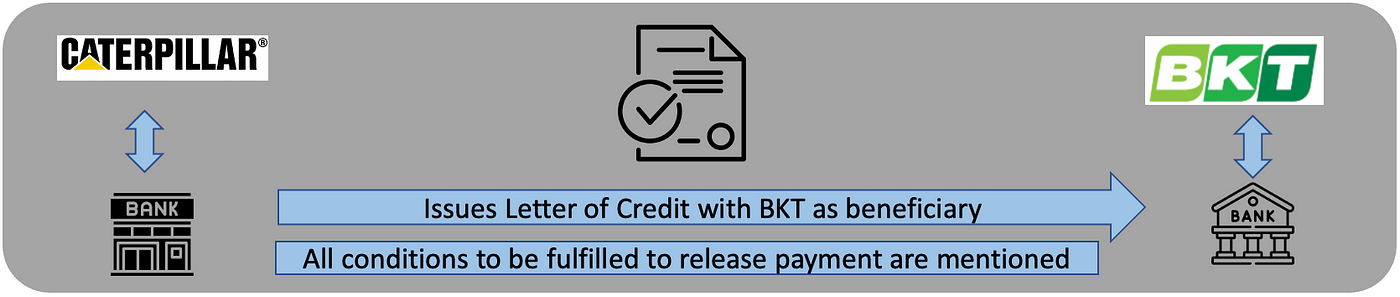

Now with this contract in hand, CAT will go to its bank (lets call it BofA, short for Bank of America) and ‘Open” an LC favouring BKT.

BKT receives this LC through its bank — say SBI- State bank of India. SBI performs a very important task here. It:

(a) Validates if the LC is genuine and is indeed issued by BofA (banks have a way of identifying each other, thanks to SWIFT).

(b) Advises BKT if BofA is a trustworthy / creditworthy bank. This is a little more complex activity, but for now we will pretend it is simple.

These are important steps, as the LC itself is an instrument that is meant to establish trust. If the issuing bank is not trustworthy, it beats the purpose. You would immediately understand what I mean if I mention CAT gets the LC issued by the Fifth Third Bank (yes, such a bank exists!). So, it is important for SBI to satisfy itself that the bank that opens the LC is indeed worthy of trust. If SBI is not able to directly establish trust, it can do so with some intermediary (called the “confirming bank”).

By doing so, SBI becomes the “advising bank” for BKT.

Now why would BofA or SBI take the trouble of doing all this for their customers? Fee income! but they will get into this business only after assessing the risk they are taking. So in a sense, the banks allow their customers to transfer risk on to them, thereby becoming trust providers.

To look at it another way, all the banks in the chain make money with LC fees. Remember, this is without lending a $, just by lending their trust (& of course managing the risk) banks make money. So this LC business -which you can see as “fee based” income in bank’s annual reports — is something banks fight for.

Let’s get back to the contents of the LC. CAT will ensure all the important conditions that are to be fulfilled are included in the LC terms & conditions for its bank to release the payment. It will include conditions like the type of tyres (Earthmax SR 47), quantity, type of packaging etc. If these conditions are met by BKT and verified by BofA, BofA will make a payment to SBI. (Did you notice that BofA is making the payment instead of CAT?).

Now, a question may pop up. Are banks equipped to validate the type of tyres? Are they qualified to ascertain the quality of materials used as per the specifications?

Banks service a wide customer base that would be dealing with a variety of merchandise. What if a pair of customers trade in chemicals; will the bank have the ability to tell what those chemicals are? Is this why bankers study chemistry in school? Or graduate in biology to validate the animal products shipped for their customers?

Thankfully, they don’t have to do all this. Banks will have to deal only with documents (without having to leave their airconditioned offices). Between trusted partners, a self-declaration by the exporter is sufficient to say what they are shipping but if an importer wants to be doubly sure, they can insist on a validation by an independent agency at the port of export, before goods are exported. They just have to ensure that this verification by the appropriate agency (identified upfront) is included in the LC conditions & a clearance certificate is one of the documents to be submitted to the issuing bank to claim payment.

Coming back to our CAT-BKT trade, all BofA has to do is, ensure BKT’s agent submits all the documents that are mentioned in the LC, with the desired contents. And if BofA is satisfied with the contents of the documents, it will release payment to SBI (for BKT).

But before that, let’s see what the steps in international trade under LC are, at a very high level.

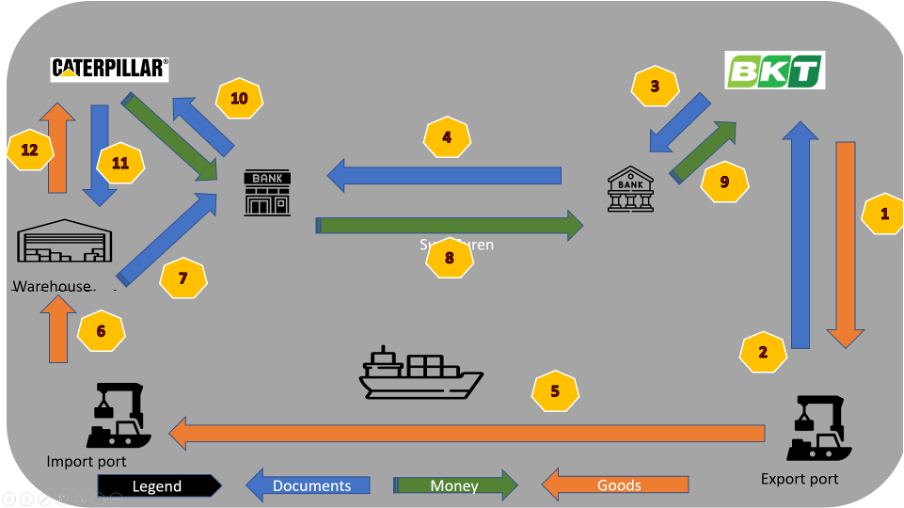

Consider the below picture, follow the numbers on the arrow for the sequence of steps. (This picture is AFTER both CAT & BKT have contracted with each other and BofA has also ISSUED the LC in BKT’s favour). In a sense the below is the actual flow of goods, documents and payments sequence. Arrows are colour coded.

Step 1: BKT sends the consignment of tyres to its freight forwarding agent, who will liaison with

(a) the export customs and get the necessary paperwork done,

(b) engage a shipping company that will take the tyres to Illinois, arrange to load them on to the ship.

(c) take out freight insurance.

Each of these entities will issue documents like export certificates, bill of lading, insurance policy etc.

Step 2: These documents are sent to BKT. The bill of lading is an important document that confirms that the shipping company has taken possession of the goods as described in the LC AND has loaded on to the ship headed towards where CAT wants.

Step 3: BKT hands over these documents to SBI, which verifies if these are as mentioned in the LC (if not, it will be iterated enough number of times to ensure they are as per the LC).

Step 4: SBI sends these documents to BofA to claim the payment.

Meanwhile, in parallel, the goods set sail to the destination port in Step 5: and are unloaded into the customs warehouse there (as in Step 6).

Step 7: All customs related procedures will be performed by CAT / its agent with the customs in the import country. Customs’ clearance & approvals are essential.

Step 8: Based on all documents (Bill of lading, Bills of exchange, Insurance, packing lists, certifications if any, etc.) that BofA has received, it takes a decision to accept or reject the payment and if accepted, they arrange to make payment to SBI as per the terms of the LC [could be immediate payment (called sight) or a deferred payment (usance)].

With this, two things happen.

(a) The transaction as per the LC is now complete from BKT / SBI point of view as their payment (or its assurance) is done. (Step 9)

(b) The title for the goods shipped are now transferred to CAT.

Step 10: All the documents that establish title to the goods and as required by the customs warehouse to release the possession of the goods are handed over by BofA to CAT, which can now share these documents to customs (Step 11) and receive the tyres (Step 12). Only at this stage CAT will get to lay its hands on the goods they purchased.

The payment terms between BofA and CAT are mutually agreed based on their relationship and upfront agreements. CAT can make the payment immediately to BofA or choose to convert the payment BofA made to SBI as a loan (much like ‘buy now pay later’), but this is between a customer and a banker as the international trade part is already complete.

BKT is happy that it received payment as long as it complied with the process and CAT is happy that payment was released only when its trusted banker verified all the documents are as per the LC conditions CAT jointly drafted.

Above is a simple flow and there are multivarious sub steps / complexities in each of the above steps. Our objective is not to get in deep but to have an overview of this process.

It is important to realise that all the communication between BofA, SBI and any banks in between are through the trusted network between banks — SWIFT.

Right from issuance of an LC to its lifecycle (issuance, additions, amendments, pre-advice, reporting discrepancies, acceptance or refusal, there are several types of messages under the MT700 series. MT stands for Message Type and each area is banking is covered by a series. 700 series (commonly written as MT 7xx) is dedicated for the LC type transactions.

Alongside, you would have also noticed (if not, please notice now), how a trusted messaging system is essential for the banking system to work and why it is important most banks in the world be part of it to move the wheels of the international trade machine.

We haven’t concluded yet as we are to see how the payment actually happens across borders. That, is a matter for our next article! See you soon.

Click on the urls below the images below to view the previous and next articles in this series

https://curiously.me/trust-trade-transact/

https://curiously.me/show-me-my-money/

Would you like to share this with someone you know? Please make use of the buttons below.

We saw how money helps in exchanging goods & services in this article. But what do our exporters do when they have to deal with buyers in countries that have their own money, issued by a different institution than ours, with a different guarantor than the one we trust.

Obviously the simplest way for an exporter is to quote a price in the currency of his home country. But it should be acceptable to the buyer (importer), for whom her home currency is different.

Why would a buyer or a seller hesitate to deal with currency which is not their home currency? Is it trust in a currency? Or is it a more practical consideration. There are two simple reasons which we will see below.

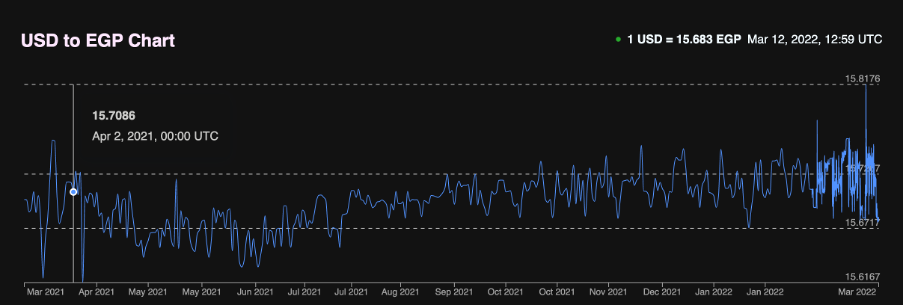

1. Stability: Imagine a carpet exporter in Turkey who prices a particular variety of carpet at 100 TRY (Turkish Lira) apiece when he sells within his own country. He would like to charge the same when he exports them too. As long as he quotes the price in TRY, there is no currency risk for him. But let’s assume the importer — who lives in Egypt- prefers not to pay in TRY and wants to pay only in EGP (Egyptian Pounds). Our exporter submits a quote in mid Dec 2021, where the exchange rate between the two currencies was 1 EGP = 1 TRY. So the carpets will be quoted at 100 EGP (which would have translated to 100 TRY). This looks simple. But we need to understand currencies can be volatile, (i.e the extent to which exchange rate varies on a given day is high). Below is a chart of exchange rate between EGP and TRY for the past one year. (Credit: xe.com)

One year exchange rate history between EGP and TRY. Credit:xe.com

Now, international trade doesn’t happen in an instant. Importers seek quotes from various exporters across countries, take their time to evaluate and then place the order. Suppose our importer in Egypt wants to place an order in mid-Jan 2022. The importer would be willing to pay only 100 EGP as that was the quoted price per carpet.

As we can see from the chart above, the exchange rate between EGP and TRY changed in Jan 2022 to 1EGP = 0.70 TRY when the deal is signed. Now if the payment were to happen immediately, our Turkish exporter would have got only 76 TRY for each of his carpets instead of 100 TRY, thereby incurring a loss if he goes ahead with the deal. All because the exchange rate was very volatile.

So just quoting the price for the order in a volatile currency is very difficult for the exporter (& to the importer if the opposite had happened). However if they were to agree to price the goods in a more stable currency, where the volatility is less, it brings some stability in the trade process. So exporters around the world want to quote the price of their goods in currencies that are less volatile. Let’s call this stable currency, XYZ for now.

2. Exchange rate risk. Let’s say our exporter “receives a confirmed order”. This means he has locked in his price in a (relatively) stable currency XYZ. This does not completely eliminate his price risk. International trade usually has a time lag between the time an order is placed and the final payment is made (more on the why in a later article) — say 3 months. There is every chance that the exchange rates between XYZ — TRY and XYZ — EGP changes in these 3 months. But this exchange rate risk can be mitigated by both the exporter and the importer by taking out currency forward contracts with their respective banks. The bank will charge a fee for this, but this mitigation gives certainty to both the importer (on how much she has to pay) and the exporter (on how much he will receive) in their respective local currencies.

A question can come in your mind, if exchange rate risk can be mitigated for a fee, why not do it at the time the quote was prepared, i.e in Dec 2021 itself? We need to remember, in Dec, there was no certainty that the importer will accept the order; so there is no cash flow expected to cover the risk. Whereas in Jan once the deal is signed, there is a contractual obligation for the importer to pay and certainty on a certain amount to be paid and received.

There will be volatility between any two currency pairs but the extent of volatility will be less if one of the currencies is a stable currency (XYZ).

Enough of talking in variables, what happens in real lives? What is the stable currency in which most trade happens in the real world? Most trade is quoted in USD (the reasons are long but the undeniable fact is, it is a currency backed by the US govt and trusted by almost the entire world to be relatively stable). A few other currencies also enjoy this trust, (EUR, GBP, JPY & CHF) but not to the extent of USD.

Lets see how the two currencies performed w.r.t USD. Below are one year historical charts of exchange rates.

First between USD and TRY. Credit: xe.com

One year exchange rate history between USD and TRY. Source: xe.com

The chart looks almost similar to the EGP TRY chart, indicating that it was TRY which had had a volatile year.

Now, if we see the exchange rate between USD and EGP in the same period, it looks like this. Credit: xe.com

One year exchange rate history between USD and EGP. Source: xe.com

The chart looks volatile but within a very narrow band. So most of the exchange rate volatility between EGP — TRY was due to high volatility of TRY and moderate volatility of EGP.

3. Fungiblity of the trade currency. While all money is fungible in theory, it has boundaries. Real fungibility happens only when the earned currency can be ‘used’ to purchase any other goods / services from a different country. Assume that our exporter quotes his goods in EGP to his Egyptian client and also receives EGP upon sale. He will now have EGP funds with him. Unless he has to buy something quoted in EGP (most likely from Egypt), he has to convert his EGP into a third currency. Take for instance that he needs to buy weaving machines from a vendor in Germany, his EGP will be of no use and he has to convert EGP to EUR which involves transaction costs and fees to bank (even if we ignore currency volatility for a moment). So exporters and importers, prefer to have a single currency that is acceptable by traders across borders.

4. Government diktat. Yes, as part of managing the economy, governments also dictate — for good reason- what currencies their international traders can deal in. This is because, governments, primarily through their central banks maintain what is called “Foreign currency reserves”, to ensure they have adequate currency to pay for their countries’ imports. Central banks cannot be holding (& maintaining) a balance in several currencies like EGP, TRY and may prefer to hold only in certain currencies (like USD, EUR, JPY etc.) that are not very volatile. (None of us would want to hold an asset ( a reserve) whose value is volatile isn’t it). Due to this, any importer or exporter of a particular country are allowed by their governments to trade in only a few currencies. Purists might want me to tell you about the gold standard, the Bretton Woods agreement of 1944, and more importantly its undoing in 1971 for why the USD is a preferred trade & reserve currency worldwide. They are correct. But we will keep it for a later day. If you are interested, you can check that out along with the concept of petrodollars. Right now I want to cover the more basic reasons as to why a stable currency is needed for trade.

Now when you zoom out and find a list of commonly preferred / allowed currencies across countries, it is a very small list and the most favoured currency is just one. And that is why, most international trade is quoted in USD.

Click on the urls below the images below to view the previous and next articles in this series

Cursory google searches would have told you what SWIFT (Society for Worldwide Interbank Financial Telecommunication) is. I am not going to repeat it but will help you relate to it and tell you why it is important, briefly.

SWIFT Logo for representation purposes. Copyright with SWIFT

SWIFT is a messaging system. Yes, it is like email for banks. Only banks around the world can send and receive messages between themselves in this messaging system. And it has to be about a financial transaction. Which means they cannot exchange cute cat videos or talk about weather. Banks generally use SWIFT for asking for payment, instructing one another to make a payment, send each other confirmations of treasury or trade transactions they did amongst each other. Each message is an instruction or an important FYI that results in a financial action on the other side.

So why the big fuss if it is like an email system between banks. Open your email inbox now, yes now! See for yourself the loads of messages sitting in your inbox, junk box and spam box. Deep inside you will also see a mail from a Nigerian Prince wanting your help (payment request) to send you loads of money (Payment instruction). Smartly you ignored the message which could have otherwise costed you money and acidity.

To avoid the pesky Prince and other fraudsters, SWIFT has an elaborate system of authenticating senders and receivers of messages, which ensures that all message senders are authenticated (the banking version of a Twitter blue tick). Many of them have an added layer of identification between themselves through bilateral (key exchange) mechanisms. As a result, if a bank receives a SWIFT message, it is authentic, received from who they claim themselves to be and the message is ‘actionable’ . There are additional acccount mechanisms, but for the purposes of our understanding, suffice to say, it is a very authentic messaging system that keeps ALL SPAM out.

Reliable & Secure: “I haven’t received the email yet”. Some of us have used this excuse or know someone who has. Such excuses don’t work with SWIFT. In its 47 years of existence, SWIFT (claims that it) hasn’t lost a single message out of the billions that were exchanged in its platform. So secure is the platform that if a bank says they sent, the recipient bank would have received it.

Not only has SWIFT not lost a single message, but the platform is so secure that no one else was able to hack or gain access to messages that were not meant for them. Yes I hear that you have heard about hacks (Bangladesh central bank etc.) but these were login credentials abused instead of the SWIFT platform yielding to hackers. Again, not a single hack in almost half a century!

Some feat!

Automation: These days we live in an API driven world where our email talks to our bank, one application talks to another etc. But SWIFT has implemented automation (which it calls ‘Straight Through Processing’) for the last 20+ years. To facilitate this, SWIFT has standards and rules on how messages are to be structured, how each field needs to be filled for each business case and so forth. So, a huge portion of the millions of messages exchanged everyday have not seen human hands at all. They all have been generated by, handed off to, received by, read and acted upon automatically , by the myriad software applications in a bank [Core banking applications, Payment (product) Processors, Payment hubs, message queues and other technical jargons your friendly neighbourhood tech guy might help elaborate].

What is the big deal you may ask, RPA is a thing and a pilot too puts his plane on autopilot. Just like how the autopilot reduces human errors and saves lives, automation in SWIFT message processing reduces errors (financial — yeah your money), speeds up transactions (in most cases less than a day but not more than two) and thereby reduces cost for you as a customer of a bank.

Standard, widely used. We know countries can’t agree on political systems, can’t agree on borders between them and proudly agree to disagree on several areas. But if there has to be a stellar example of worldwide agreement on something that has held for a long time, it is the standards published by SWIFT. So in a sense, it is truly one of the very few things the world agrees on — before expelling some specified banks due to politics that is.

There is much much more to SWIFT than this article, but for someone who wants to understand what the big fuss is about, I believe this is a good starting point. Let me know your thoughts.

Would you like to share this with someone you know? Please make use of the buttons below.

To listen to an audio version of this article, please use the play button above.

—————————————————————————————————————–

This blog is an attempt to explain the world of international finance from a bird’s eye view. While it was written with a layperson audience in mind, some of my friends in this field who have read these posts, found the posts to be useful to understand the fundamentals. So if you are new to the world of international finance or are familiar with it at some level, you will still find these articles helpful to some degree.

If you are an expert and want to offer some suggestions or contribute subject matter, you are welcome and your contributions will be cherished!

A good way to understand the world of international finance is to take a scenario & see how things work. For this purpose, we will take the restrictions put on Russia by the west subsequent to its “special military operations” in Ukraine that started in Feb 2022. Remember, we aren’t taking any sides, but are using the situation to understand the world.

Some articles of this blog are standalone and can be read independently. However, if you are someone who would like to follow a structure, then you will find reading in the following order helpful.

As a first step, we need to become familiar with “what is money”. Yes we all use it, save it and grow it, but do we know what exactly it is? Read it up in Money money, who art thou?

Have you wondered how international trade works? And why most transactions in the world are performed in USD.Find out the answers in

The world of International finance works on a distributed giant machine composed of banks. Read more on how they play a role in facilitating trade across borders in Gods of Trust!

Or how the tools of international finance play a big role in Geo-Politics in The Kill Switch.

The thing with adaptive systems is -they adapt. If one of the players don’t play nice and makes a move that hurts others, everyone takes notice. A famous saying in geo-politics is, “capability is more dangerous than intent“. This is to say, when a player accumulates an advantage, whether the intent was good or malicious doesn’t matter. Because intentions can change at a moment’s notice but a capability may takes years to build. So if a country has a finger on the kill switch, some others will work on building another capability and a few others will try to make the kill switch useless. This is a relentless game. The next series of posts will look at the challengers to the current mechanism of international finance. How some are red herrings, some are just minor inconveniences and some, turn out to be more serious. In the first of the articles in this series, we see how some of the challengers have challenges.

A new kid is on the block, a money kid! It looks like its parents, but is more sophisticated. It is a simple, yet a powerful new form of money. And it seems to be blooming across the world. Yes we are talking about CBDC. What is it you ask? Find out in CBDC- A new form of money.

In, the shifting gears of cross border payments with CBDC, you will read about why several countries are implementing CBDCs and the different collaborative initiatives between countries in the world in this area.

We look at one of the most promising collaboration projects that is set to revolutionise payments in Let’s talk mBridge. Read how it reduces risk, cost & transfer time for all parties – countries in general, corporates that do business internationally and common people like us.

Supplementary articles:

These are “explainers” on some key concepts that assist the understanding of the main theme will also appear in this blogpost. They can be read anytime or as a supplement to the main ones.

Like the one on the SWIFT network at the below link.

Leave a Reply