When we visit a store to buy a product, we ‘see’ the product, ask for a quote, if satisfied about the product and quote, we buy it (of course, we will haggle if possible – over the price). Once we pay, the transaction gets completed.

Here the quote, trade and payment transaction happen almost simultaneously. There is an element of trust which we don’t often realise. It is the trust that, we, as a consumer have, that the shopkeeper will allow us to take possession of the product upon payment. Similarly the shopkeeper trusts that the payment will be made when the product is handed over.

When we order an item online in an unfamiliar website, we don’t ‘see’ the product itself but only a representation of it on the website. Having made the payment, a question lingers in our minds: “will the product come through as promised”? Or will I receive a brick in the mail. To overcome this, we choose from a set of “risk mitigation” activities:

(a) order ‘Cash on Delivery’ — so that we don’t have to pay if the product is not delivered to our satisfaction. Or

(b) order from a renowned website (like Amazon) that ensures a return if the product was either not delivered or was not as listed.

In cash-on-delivery, there is absolutely no risk for the buyer, however the seller bears several risks. He wouldn’t know if the buyer would accept and pay for the product and still needs to pay for the transportation if the product is returned by the prospective buyer. While the seller may not lose the product itself, there is a transportation cost involved. If the product is a perishable item (like a block of cheese), the possibility that it can perish in the back and forth journey and lose its entire value is real.

What a reliable platform like amazon does is, it brings trust for both parties with its robust return policy and feedback mechanism on products and sellers. Both buyers and sellers recognise this value addition by Amazon (or a similar service) and make long distance trade possible and vibrant — whether we are conscious about it or not.

This element of ‘Trust’ becomes even more pronounced if the trade is international — where additional transit times and customs complications are usual. Yet billions of goods and services get sold and bought across the oceans. Is there an Amazon like entity that provides trust? Well, it is not one single entity a network of banks (yes banks!) that provide this trust.

Let’s take an example of a trade between two very reputed, financially rock-solid and ethical companies. I say this because none of these companies will wilfully cheat the other and pose a credit risk to the other.

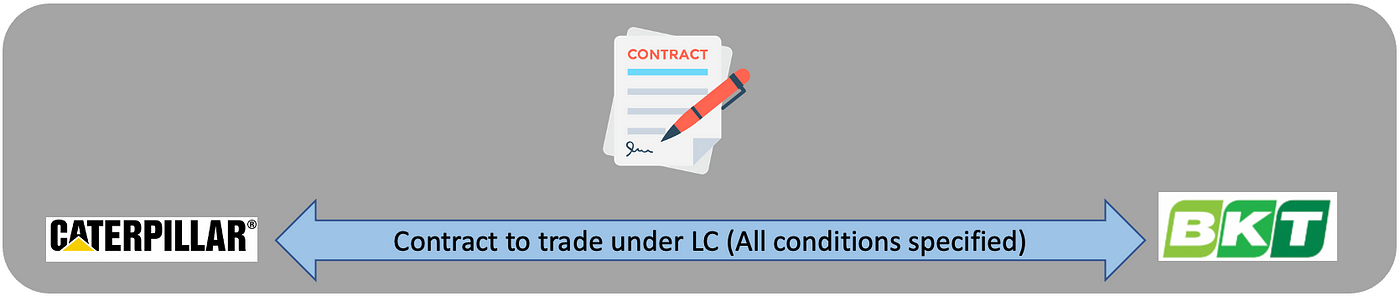

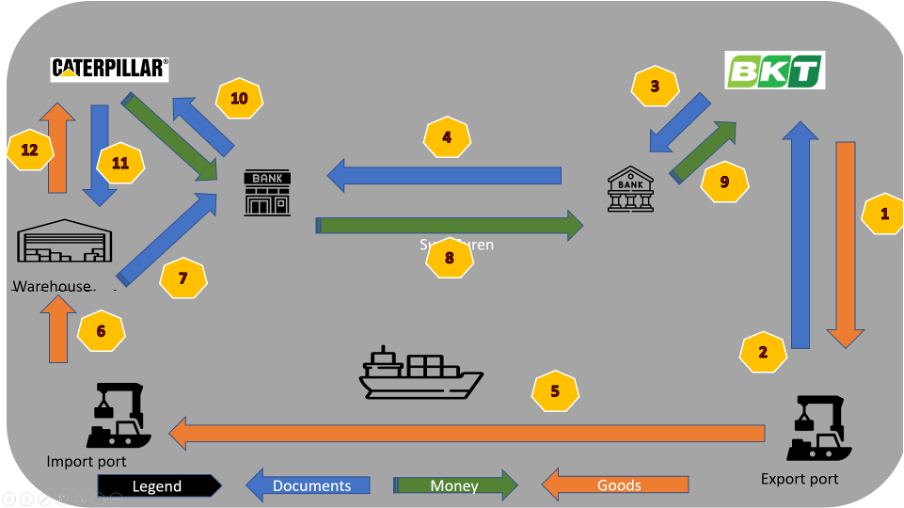

Caterpillar USA, (the manufacturer of those monster trucks we all love) and Balkrishna Industries Ltd., (India’s largest manufacturer of off-highway-tyres) sign a deal where BKT is to supply its famed “Earthmax SR 47” tyres for one of CAT’s off-Highway trucks. BKT has its plant in the western Indian state of Gujrat and CAT needs those tyres in Illinois, US to be fitted into those (monster) trucks.

The journey of those tyres, even before they start their journey moving trucks on the road, is a long one — inside containers from BKT’s plants in Gujarat, India by road to one of the ports in Western India, then by sea to the eastern seaboard of US and then again by road to Illinois. CAT will pay BKT only if the tires (since they have reached American shores, lets use the American spelling) it receives are of the specification they asked for and if the tires reach them in good shape. The journey of the Earthmax tires can be interrupted in the sea by storms, sea pirates off the coast of Somalia or even delayed by a random ship that runs aground in the narrow straits of Suez canal. Bottomline, the tires may not arrive at the warehouse of CAT in time, despite the best intentions of BKT.

Or, in spite of supplying the right tires braving all the interruptions on the way, BKT may not receive payment for what it delivered to CAT because — ahem, a political sanction was put in place due to one of those unforeseen risks we are slowly getting used to in these uncertain times.

These are risks that both the companies face!

As commercial public limited companies that need to answer their shareholders, these companies will employ the best international trade practices to de-risk. Enter — banks & their “Letters of Credit”.

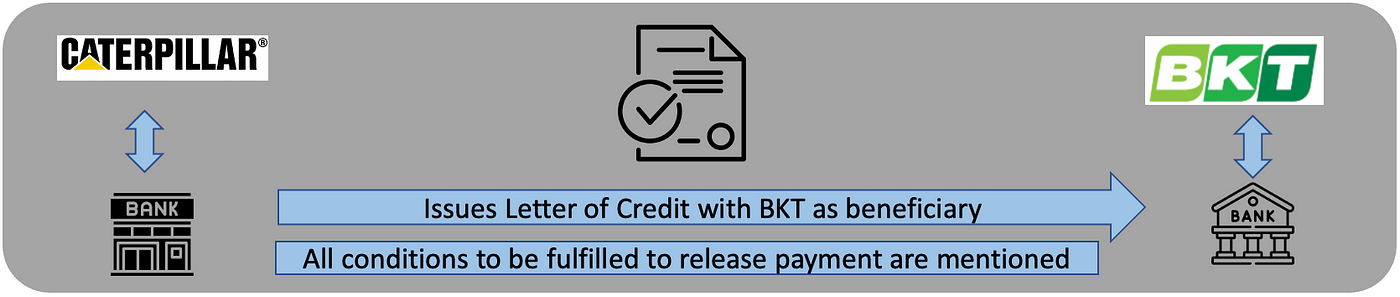

In its simplistic terms, a letter of credit is an assurance by a bank that it will make payment to an exporter, as long as the exporter supplies the goods according to the terms agreed between the exporter and importer, at the agreed place.

If BKT indeed made available to CAT the tyres of agreed quality & quantity at the agreed place and provides documentation proving that, CAT’s bank will pay BKT’s bank to be credited to BKT.

And if BKT isn’t able to do that, CAT is protected and no money is paid to BKT.

Voila! We now have a mechanism of instilling trust in a trade between two companies across the oceans. Actually, this mechanism has been in place for decades — even before Amazon came into the picture.

Thus banks provide a very important ingredient (apart from money of course) — the trust needed for international trade & transactions.

Photo Credits:

Picture collages made from pictures & photos thanks to:

- Photos by krakenimages & Ian Taylor on Unsplash

- Photos by Mediamodifier & Coker free vectors on Pixabay

- Photo by energepic.com through pexels.com

- logos of respective companies

Click on the urls below the images below to view the previous and next articles in this series

Leave a Reply