It was 1995, present in the middle of Yellowstone national park, in the US, was a beautiful & scenic valley. Miles and miles of panoramic treeless land, dotted with shrubs and small plants. Beautiful spotted deer were browsing the plants and grazing the grass. There was silence, not even the sound of the wind rustling the trees as there weren’t any trees around. There was silence, No sound of flowing streams that are usually found in a forest, for there weren’t any. There was silence, as there weren’t any animals apart from the deer.

Suddenly, out of nowhere come a pack of wolves which makes the deer scatter like an explosion.

The pack of wolves target a single deer, chase it, spring on it and snap at it from all sides.

The deer falls pathetically, its hooves drumming the ground in a frantic hope for survival. One of the wolves strangles its neck and in less than a minute, all is over and the wolves have their meal.

Who is the villain here?

Yellowstone was not a natural habitat for the wolves. They were introduced into it in 1995 as part of a science experiment called “rewilding”.

A few days and a few more hunts later, the deer learn from experience and radically change their behaviour. They start to avoid the places where they could be trapped by the wolves– the valleys, the gorges and the ridges.

With no deer to stop vegetation growth, these places start to regenerate. The height of the trees increase 4 times in just a year, leading to a traffic of birds, bees and beavers. The bees help in pollination, the birds help spread the seeds of trees far and near and the beavers build dams of water along the small streams which bring in fish, reptiles and amphibians. The area explodes with life!!

Barren valleys grow to be forests. Then come the large birds like eagles and vultures. The rivers have more water and because of the new forests coming in their way, rivers change their courses. Vegetation grows and stabilises soil erosion. In just a matter of few years, the entire ecology of that part of the Yellowstone national park changes into a wild forest, a noisy forest, a very wet forest. Wild with a variety of flora & fauna, noisy with the cacophony of bird calls & insect songs and wet with rains and streams and rivers.

All because of a small pack of wolves and a few herds of deer less.

Now with this sequel to the initial story of the hunt, our initial judgement of the wolves being the villains of the story change and the possibility that the deer aren’t saints either, dawns on us.

It is very easy to fall for the drama and unduly make a villain out of the wolves when the deer were doing the same thing to the plants and shrubs. They stopped what could have been a thriving habitat for several flora and fauna.

If you look at the big picture, you could say both were villains or if you put in some perspective, both of them were not villains, they were just eating their food. They were just trying to survive, and the only difference was that the wolves’ way of bringing food to the table was more dramatic in our eyes!!!

That brings us to the crux of this post. The above real-life story was to highlight how drama hijacks our normal thinking process. Not just here, but everywhere a sense of drama clouds our judgement and we could take wrong decisions.

We need to be dispassionate in decision making in our everyday lives. We vote the wrong person falling for an impassioned speech, or choose a wrong partner at an emotional moment. We could make bad investment choices based on an entertaining presentation or quit a company because we are angry with the boss. This power of drama / stories / narratives are very well exploited by companies in their advertisements. The next time you see an advertisement, pause to reflect if it was about the products’ features or its benefits or was it just an emotional story to make you feel a particular way. I am not advocating you to be a callous calculating machine, but at least take a moment to reflect without emotions before you make an important decision.

Emotion is temporary, while the decisions you take could be permanent.

Beware that an emotional decision is not always the right decision. In such circumstances, we could be our own villains & victims. So the best way to avoid these traps is to defer decision making until we clear our heads and are ready to be objective.

Picture credits: Forest picture is a Photo by Luca Bravo on Unsplash & the stream picture is a Photo by Amit Godase on Unsplash.

Would you like to share this with someone you know? Please make use of the buttons below.

Something we all do, but understand so less about. Not we aren’t talking about anything fancy, just sleep! What is it, why we need it and some fascinating animal behaviour around sleep in this article.

Did you get conned in recent times by a trickster? Did you think such tricksters abound only amidst humans that are a supposedly advanced species? Think again. Several animals do this, even to us? What exactly happening when animals put on their camouflages? Read and share your thoughts in this article that puts forth some alternate arguments.

The natural world offers some lessons on decision making. From drama in the wild to advertisements that get our attention, this article offers some suggestions on when to decide and when not to.

Most movies are for entertainment, but some are lessons. Here is a review of one such movie that helps us understand human nature, science, scientists and politicians with a bomb.

Would you like to share this with someone you know? Please make use of the buttons below.

A few years back, the then youngest CEO of SAP India, Ranjan Das, a fitness freak, a marathon runner, came home from his usual workout at the gym, and collapsed of a massive heart attack.

How can someone who was athletic, at the pink of his health and in top form, die of heart attack? The reason? He didn’t sleep enough.

In today’s fast paced world where time is at short supply, the first activity we cut short on, is sleep. So let’s attempt to understand about sleep a little more: why we sleep, how much sleep is enough, what are the effects of lack of sleep and how to sleep better.

During the time we sleep, we don’t eat, we don’t work, we don’t play, we don’t have sex, we don’t seem to be doing anything worthwhile and hence at first glance, sleeping appears to be a complete waste of time. But we all sleep, every single day.

It is not just humans that sleep, all mammals and birds sleep too. Even small animals that are at risk of losing their lives to their predators while asleep, also sleep. Why do they need to sleep at such high risk to their lives? Normally evolution would have weeded out such species as part of natural selection. But it hasn’t happened, pointing to the importance sleep plays in every life form.

Dolphins, which are closer to human beings are not like other fish. They breathe air like us through the blowholes on top of their heads. Which means, they need to periodically surface from water to breathe. But how do they breathe when they sleep? Without any predator they might die simply because they slept when they had to breate!! But we know dophins don’t die in their sleep. How do they do it? To manage this, they sleep one half of the brain at a time called unihemispherical sleep. One hemisphere of their brain sleeps while the other stays alert. And then the cycle alternates. They sleep in pairs such that the alert part of their bodies (since each hemisphere of the brain controls one half of the body) are on the outside, to keep an eye on predators and synchronise their surfacing to breathe.

Dolphins courting? No they are sleeping partners, each helping the other to sleep during the night.

A few other mammals like bats, seals, some long distance migratory birds and owls also demonstrate unihemispherical sleep.

Why did nature go to such lengths to ensure we sleep?

That’s a question scientists have been trying to answer for several years now. Despite the years of scientific research on sleep, our understanding of sleep is very basic even today.

When asked why we sleep, Dr William Dement – called the Father of Sleep Medicine – who was also the Founder of Sleep Research Centre at Stanford says

“We don’t really know. We sleep in order to not be sleepy otherwise”

Dr. Clete Kushida, the Medical Director, Stanford Sleep Medicine Centre, after years of research since the 1970s also says he still doesn’t know.

But there are a dozen theories, let’s see the three most popular ones

We sleep to conserve energy. Our brain is only 2% of our body weight but uses 20% of the energy. To provide this, our brain shuts down active bodily functions [it literally paralyses our muscles to keep us still] during sleep and uses the energy for itself.

Body restores itself during sleep. Muscle growth, tissue repair, protein synthesis – all happen through an orchestra of hormones that create a symphony of events during our sleep. In simple terms, various toxins are flushed out and we grow during our sleep

Brain processing and memory consolidation –the filing of events, making them available when needed and using them to handle similar situation – in short this is intelligence. So during sleep, brain does the housekeeping to keep us intelligent. Empirical evidence suggests that if you sleep well, you are three times more likely to be creative.

Okay, so what is the right duration of sleep. Is it 6 hrs, 7 hrs? 8?, 9? How much is good enough. There is no consensus, but adult humans need at least 6 hrs of sleep at a stretch. A good empirical measure is, if you don’t feel sleepy during the day until your next regular sleeping time, then that sleep duration is adequate for you.

Lack of sleep leads to mental, emotional & physical fatigue, depression, obesity and lower life expectancy.

On days following sleepless nights, high levels of cortisol accumulate in your body which leads to stress related disorders like cardiac ailments and diabetes. Sleep loss produces Grelin, which makes you seek carbohydrates and makes you obese. In short, chronic lack of sleep sets in motion a series of irreversible ailments that ruin our long-term health.

So how to get good sleep. If you have trouble getting good sleep, what can you do? Not much but a few things help.

Keep a regular sleep schedule

Exercise helps

Limit Caffeine and alcohol, if unavoidable, don’t drink too close to sleeping time

Turn off lights and keep the room as dark as possible.

Keep mobiles away – even if you are only browsing it, the light from the mobile is troublesome.

Your life is a reflection of how you sleep , and how you sleep is a reflection of your life!. If you sleep well, you live better. So wake up to sleep facts my friends. Lack of sleep can kill!!!

Would you like to share this with someone you know? Please make use of the buttons below.

To listen to an audio version of this article, please press the play button above.

————————————————————————————————————————————

Let’s start with answers to the questions posed in the previous article.

Q1: In this entire chain of cross-border payment transaction- where a company in India paid a company in Saudi Arabia, in which leg did the money actually move?

A: Money actually moved from one bank in the US to another in US. It did not cross any border!

But wasn’t this supposed to be a cross border payment? Money from India to Saudi?

Indeed! But because the payment was in USD, the transfer happened between two NOSTRO accounts in the US itself.

But what crossed borders, if money didn’t?

Messages! Yes just messages went beyond borders.

So if Adam Savage (of the popular TV show “Mythbusters”) were to investigate this, he would proudly proclaim – Busted!!

Contrary to popular perception in cross border payments, money doesn’t cross borders, only messages do.

But the companies in India and Saudi didn’t have USD accounts, they had INR and SAR accounts. Surely there must have been some conversion that must have happened?

Yes, that’s brings us to question no 2.

Q2: Where exactly did the currency conversion from INR to USD or USD to SAR happen?

In their respective countries.

INR- USD was done by SBI Mumbai and USD -SAR was done by AL Rajhi bank, Riyadh.

The banks in US don’t determine the exchange rate for any of the legs of this particular transaction.

Q3: Which countries’ compliances and regulations had to be applied in this transaction?

It is easy to guess that the compliance of governments in India and Saudi Arabia apply to these transaction as the buyer and seller are in these respective countries.

But here is the kicker. Just because the payment passes through banks in US, the compliance rules of the Govt. of the US of A also apply to this transaction.

If we zoom out of this single transaction and have a satellite’s eye view (a bird wouldn’t have so much of a span for our purposes), since most international trade happens in USD, ALL (yes all!) of those transactions have to comply with the rules of the Govt. of US of A.

-we can say that, just because USD is the world’s popular trade currency, central banks around the world buy and store it as a major reserve currency, thereby increasing the demand for USD perennially.

-the US govt is able to apply it’s writ on international transactions between two random foreign entities that are thousands of miles away from the shores of US, despite the fact the goods don’t come anywhere near the US.

Is this a good thing or a bad thing? Depends!

Depends on where you stand or how friendly one or both of the trading countries are with the US of A.

Let’s take just two examples to see the impact of this.

FATCA. Citizens of almost all countries around the world had to declare their FATCA status with banks around the world. Why? Because the US govt said unless each bank (called an FFI – Foreign Financial Institution) in every country collected and reported relevant data to the US on their FATCA status, US govt will withhold 30% of the value of bank’s qualifying (this is a subset of all txns) transactions going through US, done for FATCA non-compliant customers living in a foreign country. Considering almost all major banks around the world need to have USD NOSTRO accounts with banks in US, they have no choice but to comply.

FATCA (Foreign Asset Tax Compliance Act) is a US law since 2010 to track the income from the foreign assets of US citizens, living and maintaining accounts abroad. These assets could be Savings or fixed deposits in banks, Mutual Funds, Insurance products, real estate etc. As an example, if a US citizen has an account in Italy, the US govt wants to know. While most govts ask their citizens to declare their foreign assets and income voluntarily, the US govt goes one step further. It asks the banks’ and financial institutions of other countries to report, if any of the accounts they service for their customers, are for US citizens. To know this, the banks need to ask ‘every’ account holder to give a declaration of their US citizenship status.

With the US Dollar’s unique position of being an international trade currency, US was able to enforce compliance on every financial institution in 90 countries of the world, for an internal tax program. Who bears the operational costs and inconvenience of this compliance? – the respective banks. Who will the banks recover this cost from? Their respective customers. So here is an internal tax compliance program of the US govt, being paid for and complied with, by citizens of other countries around the world.

The second example is what happened as part of sanctions on Russia following the Ukraine-Russia war. US was able to successfully stall all (well, almost all) international trade if one of the trading partners was a Russian entity.

How is this even possible? Recall the organisation and messaging platform called SWIFT? And that it is owned by banks across Europe and US. (you can read more about SWIFT here). Also, if you recall the details of the SWIFT message in this article, you will know that every SWIFT payment message contains information on who originated the payment and who the beneficiary is. Combined with the fact that each USD transaction will have to go through banks in the US, it is easy for banks in the US to know who are the entities in an international transaction. As a result, the enforcement of this ban was quick, because US banks had a switch to identify and kill transactions, if one of the trading parties was Russian.

We need not get into the merits of the war or the sanctions. But if you look at it purely from a risk manager’s point of view, any country is at risk of immediate suspension of its international trade if they fall out of favour of the US. In that sense, the kill switch to the world’s international trade is in the hands of a few western nations.

Isn’t this a risk for other behemoths of international trade? like say – China? Yes and that’s why they try to wean away their international transactions from USD and are promoting Yuan based transactions. Or even trade based on bilateral currencies between China – Saudi Arabia, China- Iran, China- Russia (that’s no surprise). But it is not easy, because it is not just in the realm of economics or trade, but a matter of geo-political dominance. This game has had its players and many haven’t lived to tell their story.

There has been a recent challenger to this – albeit a tiny one- having some acceptance across countries, including the USA. You must have heard about Bitcoin and its cousins. These are & will be limited to miniscule, marginal, esoteric or arcane transactions and will not enter the mainstream as a force to reckon with.

But a bigger challenger is on the slow brew. The war that has already started in eastern Europe, and more wars that are about to start, are a reaction to it. Lets cover that in the next article.

Click on the urls below the images below to view the previous and next articles in this series

Let’s see at a high level how an international transaction happens. This time, we will use the most popular commodity transaction -oil — in our illustration.

The trade: In our example, the largest private sector refiner in India — Reliance Industries Ltd. (RIL hereafter) buys oil from Saudi Aramco of Saudi Arabia (we will refer to this as Aramco from here on). RIL banks with SBI, Fort branch, Mumbai and Aramco with Al Rajhi bank in Riyadh.

Most oil in the world gets sold in USD for the various reasons we saw in this article. Which means both buyer and seller will have to necessarily settle through a bank in US of A, irrespective of where they are. In our case, even though the seller is from Saudi Arabia and the buyer is from India, and the oil they exchange will never touch the shores of US of A, the commodity is priced in USD.

We can recall that the transaction will most likely be under the “letter of credit” and will involve the below parts.

LC Process: Before placing an order with Aramco, RIL will approach SBI to “Open” an LC favouring Aramco. Aramco will furnish it to its bank Al Rajhi and ask if the LC is trustworthy. If Al Rajhi is not comfortable with SBI’s trustworthiness or if their bilateral limits are exhausted, Al Rajhi can ask another bank to “confirm” SBI’s trustworthiness. By confirming this LC, this intermediate bank (say Citibank Riyadh) acts as a guarantor for SBI.

Since the transaction is to exchange Oil for Money, there are two Settlements. Since we have already seen the goods settlement in detail in the previous article (linked here), we will see how the money settlement happens in more detail here:

Goods settlement: When the ship calls on the port and unloads to the customs’ warehouse / oil farm, RIL, by sending an “acceptance” through SBI, gets the title for goods in the port / and lifts the goods. The payment terms can be on “Sighting” the goods — i.e pay the money and take the goods, or agree to pay x days after “accepting” to pay. The payment terms are as agreed upfront between the trade partners RIL & Aramco.

Money settlement: Since the transaction is in USD and as both SBI Mumbai and Al Rajhi, aren’t present in USD settlement zones, both of them need correspondent banks in the US of A to settle their transaction.

What are correspondent banks? These are banks where other banks maintain accounts — most often in a foreign country and in the currency of that country. So in our example, let’s say SBI Mumbai’s USD correspondent bank is SBI New York and Al Rajhi’s is JP Morgan Chase NY. By design these correspondent banks will be in US of A because that is where USD settlement happens. This correspondent relationship is not a transient one for ‘a’ particular transaction but are pre-established relationships between banks for long term. In fact, correspondent banks are listed publicly in a bank’s website and also figure in directories bankers use among themselves.

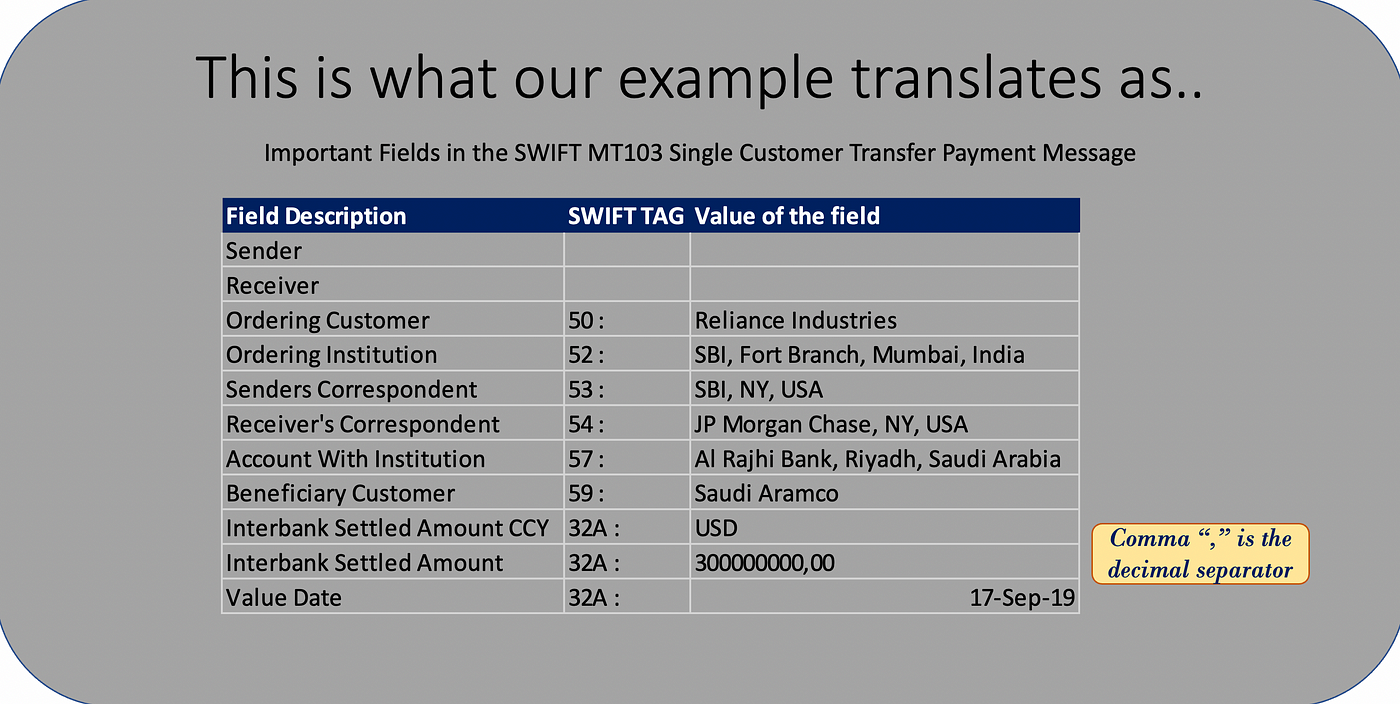

Now, back to our transaction. Here are the different parties in payment parlance. Note the banks are identified with their SWIFT BIC (Bank Identification Code, a unique code for each bank + branch combination, which will direct the SWIFT messages to them, like an email is sent to an email address) • Ordering Customer (the one who initiates the Payment): Reliance Industries • Ordering Institution (the bank that sets in motion the payment process within the banking system): SBI, Fort Branch, Mumbai SBININBB689 • Beneficiary of the Payment: Saudi Aramco, Saudi Arabia. • Account With Institution (the bank where the beneficiary holds an account): Al Rajhi Bank, Riyadh, RJHISARI • Sender’s Correspondent (the USD correspondent of the bank that sends the payment message): SBI New York, SBINUS33 • Receiver’s Correspondent (the USD correspondent of the bank that receives the payment message): JP Morgan Chase New York CHASUS33

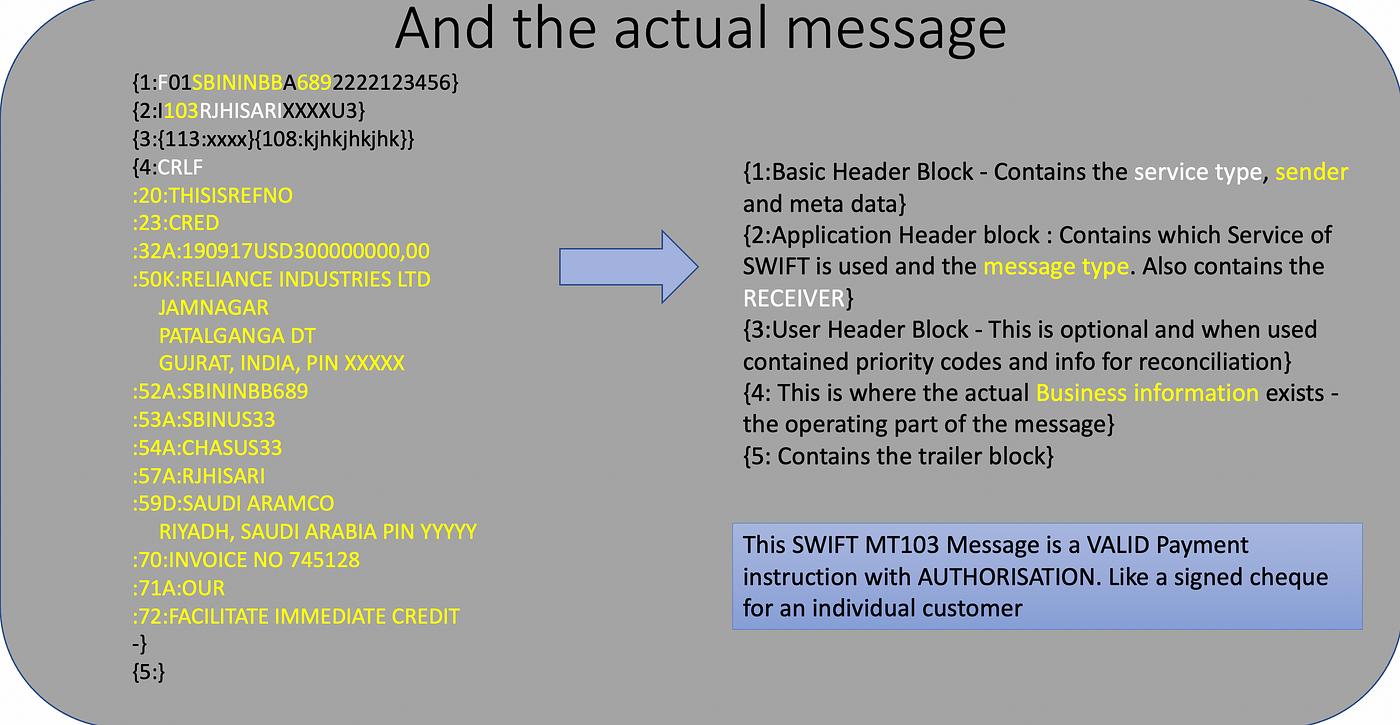

Each of these parties are identified in specific slots (called TAGs) in the respective SWIFT messages. For example the MT 103 message in our example will look like this.

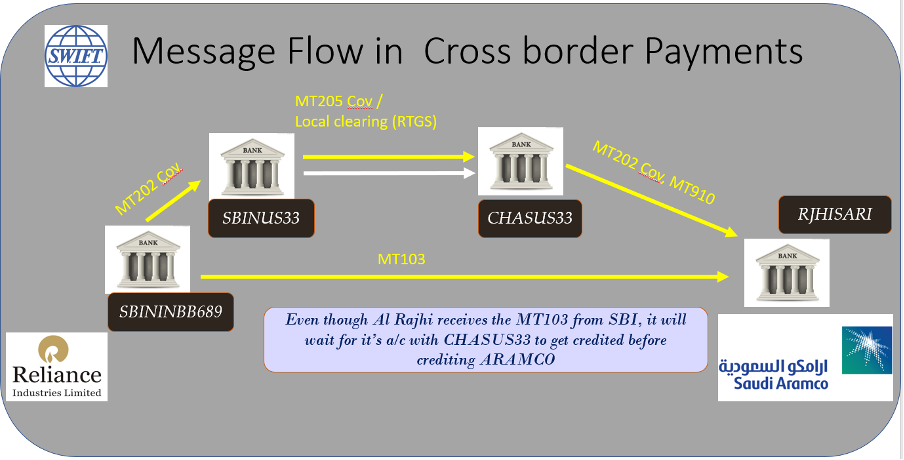

When RIL asks SBI Mum to pay, say USD 300 Mn to Aramco’s a/c held with Al Rajhi, Riyadh, the payment will happen like this.

1. SBI Mum (SBININBB689) will send a (SWIFT MT103) message to Al Rajhi (RJHISARI) saying that it is arranging payment through

the mentioned correspondent banks and that is against specific invoice number 745128. This MT 103 is a “Customer payment message”. Which means there is a customer on behalf of whom the payment is initiated.

2. SBI Mum will “inform” SBI New York (SBINUS33) through SWIFT MT 202COV to pay Al Rajhi’s a/c with JP Morgan Chase New York, with specific account number details.

Couple of clarifications here:

How would SBI MUM know who is Al Rajhi’s USD correspondent or even the account number? Aramco would have shared this with RIL, which in-turn would relay it to SBI MUM. Even without Aramco telling them, the USD correspondent would be available in commercially available directories in the market that all banks subscribe to. These are like the yester-year telephone directories that give the different correspondent banks of most banks in the world in each currency.

What is this MT202COV? It is a message type to be used when a bank instructs its correspondent bank in a foreign country to move funds from its own account, to complete a customer payment it initiated. This type of payment mechanism is called the ‘Cover” method and hence the “COV” next to the message type MT202. Banks send similar messages to their correspondents for their own purposes as well. In such cases they will simply use the message type MT202. I elaborate this to highlight how robust the SWIFT system is, which covers different scenarios of business and in-turn promotes its wide-spread acceptance, automation and even standardisation. To this date, SWIFT is the de-facto platform for transactions among banks across borders.

3. With the above information, SBI NY will transfer the funds to JPMC in the local clearing in US — either CHIPS or FEDWIRE. To inform JPMC that this is an intermediate step in an international payment emanating from India and that both SBI NY and JPMC NY are just cogs in this wheel of international payment, SBI NY will relay the payment details through a SWIFT MT 205 COV message.

MT205 is similar to MT202 except that 205 is sent between banks when the currency of transfer is a local currency for both the banks. Since USD is the local currency in US where SBI NY and JPMC NY operate, MT205 is used.

Now we come to the last leg.

4. Once Al Rajhi sees a credit in its account with JPMC, meant for Aramco, they will pass on the credit to Aramco. Else they will wait for a confirmation message from JPMC. This can come as another set of SWIFT messages — MT 202 COV or a Credit advice (called an MT 910). Only after this we can say the transaction can be said to have been “settled” i.e the cross-border payment transaction is said to be complete!

The reason I explained the above in detail is to set you thinking. Let me leave you to ponder over the below questions.

In this entire chain of cross-border payment transaction- where a company in India paid a company in Saudi Arabia, in which leg did the money actually move?

Where exactly did the currency conversion from INR to USD or USD to SAR happen?

Which countries’ compliances and regulations had to be applied in this transaction?

Once you have had time to think and have some responses, I will cover the answers and the impact in the next article.

When we visit a store to buy a product, we ‘see’ the product, ask for a quote, if satisfied about the product and quote, we buy it (of course, we will haggle if possible – over the price). Once we pay, the transaction gets completed.

Here the quote, trade and payment transaction happen almost simultaneously. There is an element of trust which we don’t often realise. It is the trust that, we, as a consumer have, that the shopkeeper will allow us to take possession of the product upon payment. Similarly the shopkeeper trusts that the payment will be made when the product is handed over.

When we order an item online in an unfamiliar website, we don’t ‘see’ the product itself but only a representation of it on the website. Having made the payment, a question lingers in our minds: “will the product come through as promised”? Or will I receive a brick in the mail. To overcome this, we choose from a set of “risk mitigation” activities:

(a) order ‘Cash on Delivery’ — so that we don’t have to pay if the product is not delivered to our satisfaction. Or

(b) order from a renowned website (like Amazon) that ensures a return if the product was either not delivered or was not as listed.

In cash-on-delivery, there is absolutely no risk for the buyer, however the seller bears several risks. He wouldn’t know if the buyer would accept and pay for the product and still needs to pay for the transportation if the product is returned by the prospective buyer. While the seller may not lose the product itself, there is a transportation cost involved. If the product is a perishable item (like a block of cheese), the possibility that it can perish in the back and forth journey and lose its entire value is real.

What a reliable platform like amazon does is, it brings trust for both parties with its robust return policy and feedback mechanism on products and sellers. Both buyers and sellers recognise this value addition by Amazon (or a similar service) and make long distance trade possible and vibrant — whether we are conscious about it or not.

This element of ‘Trust’ becomes even more pronounced if the trade is international — where additional transit times and customs complications are usual. Yet billions of goods and services get sold and bought across the oceans. Is there an Amazon like entity that provides trust? Well, it is not one single entity a network of banks (yes banks!) that provide this trust.

Let’s take an example of a trade between two very reputed, financially rock-solid and ethical companies. I say this because none of these companies will wilfully cheat the other and pose a credit risk to the other.

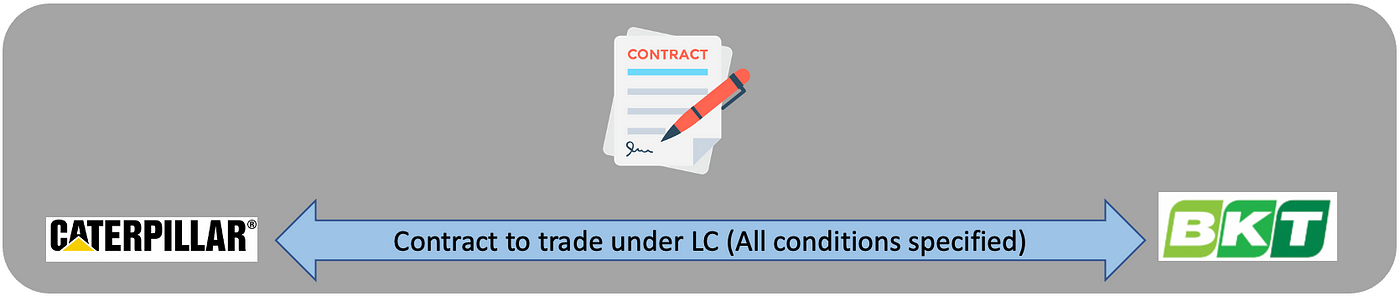

Caterpillar USA, (the manufacturer of those monster trucks we all love) and Balkrishna Industries Ltd., (India’s largest manufacturer of off-highway-tyres) sign a deal where BKT is to supply its famed “Earthmax SR 47” tyres for one of CAT’s off-Highway trucks. BKT has its plant in the western Indian state of Gujrat and CAT needs those tyres in Illinois, US to be fitted into those (monster) trucks.

The journey of those tyres, even before they start their journey moving trucks on the road, is a long one — inside containers from BKT’s plants in Gujarat, India by road to one of the ports in Western India, then by sea to the eastern seaboard of US and then again by road to Illinois. CAT will pay BKT only if the tires (since they have reached American shores, lets use the American spelling) it receives are of the specification they asked for and if the tires reach them in good shape. The journey of the Earthmax tires can be interrupted in the sea by storms, sea pirates off the coast of Somalia or even delayed by a random ship that runs aground in the narrow straits of Suez canal. Bottomline, the tires may not arrive at the warehouse of CAT in time, despite the best intentions of BKT.

Or, in spite of supplying the right tires braving all the interruptions on the way, BKT may not receive payment for what it delivered to CAT because — ahem, a political sanction was put in place due to one of those unforeseen risks we are slowly getting used to in these uncertain times.

These are risks that both the companies face!

As commercial public limited companies that need to answer their shareholders, these companies will employ the best international trade practices to de-risk. Enter — banks & their “Letters of Credit”.

In its simplistic terms, a letter of credit is an assurance by a bank that it will make payment to an exporter, as long as the exporter supplies the goods according to the terms agreed between the exporter and importer, at the agreed place.

If BKT indeed made available to CAT the tyres of agreed quality & quantity at the agreed place and provides documentation proving that, CAT’s bank will pay BKT’s bank to be credited to BKT.

And if BKT isn’t able to do that, CAT is protected and no money is paid to BKT.

Voila! We now have a mechanism of instilling trust in a trade between two companies across the oceans. Actually, this mechanism has been in place for decades — even before Amazon came into the picture.

Thus banks provide a very important ingredient (apart from money of course) — the trust needed for international trade & transactions.

Photo Credits:

Picture collages made from pictures & photos thanks to:

Photos by krakenimages & Ian Taylor on Unsplash

Photos by Mediamodifier & Coker free vectors on Pixabay

Photo by energepic.com through pexels.com

logos of respective companies

Click on the urls below the images below to view the previous and next articles in this series

Now that we understand the need for trust and how “Letters of Credit” (we will call this LC from here on) bridge the trust deficit among (relatively) unknown trade partners, let’s get into the mechanism of how they work.

Let’s carry on with the previous example of our fictitious trade between Caterpillar & BKT tyres.

Once CAT and BKT find each other suitable (for the transaction that is 😁 ), they enter into a contract that will determine

– what type of tyres BKT is selling, its technical specifications

– the quantity

– price,

– what does that price include (just the products, or freight & insurance too)

– where will it be delivered (at CAT’s location or is it sufficient if BKT delivers it to someone outside its own factory)

– when the tyres will be shipped / delivered

– how will the trade be carried out (through LC)

– which banks will be involved and who pays the fees

– how many days does CAT get to make the payment once the invoice is served

– any inspections to be done by a third party at the port where the tyres will be offloaded?

– Anything else they both (CAT & BKT) agree on.

So, in a sense, each and every foreseeable part of the transaction will be committed in the contract — including unforeseeable “force majore” clauses.

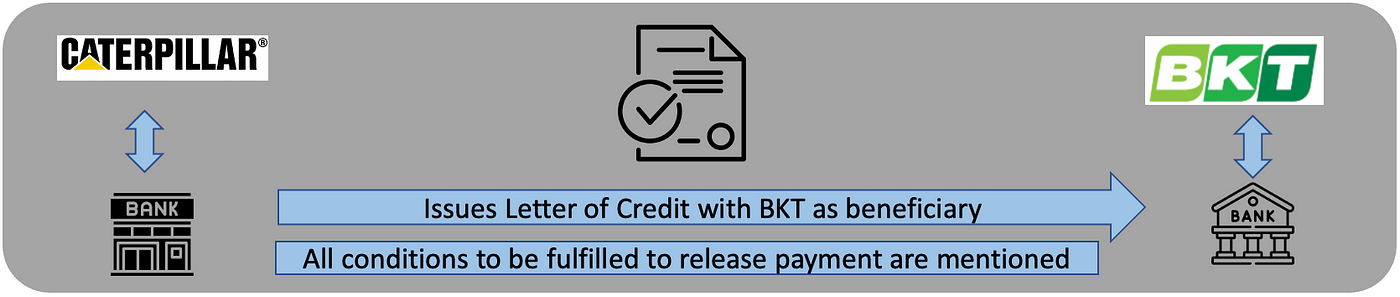

Now with this contract in hand, CAT will go to its bank (lets call it BofA, short for Bank of America) and ‘Open” an LC favouring BKT.

BKT receives this LC through its bank — say SBI- State bank of India. SBI performs a very important task here. It:

(a) Validates if the LC is genuine and is indeed issued by BofA (banks have a way of identifying each other, thanks to SWIFT).

(b) Advises BKT if BofA is a trustworthy / creditworthy bank. This is a little more complex activity, but for now we will pretend it is simple.

These are important steps, as the LC itself is an instrument that is meant to establish trust. If the issuing bank is not trustworthy, it beats the purpose. You would immediately understand what I mean if I mention CAT gets the LC issued by the Fifth Third Bank (yes, such a bank exists!). So, it is important for SBI to satisfy itself that the bank that opens the LC is indeed worthy of trust. If SBI is not able to directly establish trust, it can do so with some intermediary (called the “confirming bank”).

By doing so, SBI becomes the “advising bank” for BKT.

Now why would BofA or SBI take the trouble of doing all this for their customers? Fee income! but they will get into this business only after assessing the risk they are taking. So in a sense, the banks allow their customers to transfer risk on to them, thereby becoming trust providers.

To look at it another way, all the banks in the chain make money with LC fees. Remember, this is without lending a $, just by lending their trust (& of course managing the risk) banks make money. So this LC business -which you can see as “fee based” income in bank’s annual reports — is something banks fight for.

Let’s get back to the contents of the LC. CAT will ensure all the important conditions that are to be fulfilled are included in the LC terms & conditions for its bank to release the payment. It will include conditions like the type of tyres (Earthmax SR 47), quantity, type of packaging etc. If these conditions are met by BKT and verified by BofA, BofA will make a payment to SBI. (Did you notice that BofA is making the payment instead of CAT?).

Now, a question may pop up. Are banks equipped to validate the type of tyres? Are they qualified to ascertain the quality of materials used as per the specifications?

Banks service a wide customer base that would be dealing with a variety of merchandise. What if a pair of customers trade in chemicals; will the bank have the ability to tell what those chemicals are? Is this why bankers study chemistry in school? Or graduate in biology to validate the animal products shipped for their customers?

Thankfully, they don’t have to do all this. Banks will have to deal only with documents (without having to leave their airconditioned offices). Between trusted partners, a self-declaration by the exporter is sufficient to say what they are shipping but if an importer wants to be doubly sure, they can insist on a validation by an independent agency at the port of export, before goods are exported. They just have to ensure that this verification by the appropriate agency (identified upfront) is included in the LC conditions & a clearance certificate is one of the documents to be submitted to the issuing bank to claim payment.

Coming back to our CAT-BKT trade, all BofA has to do is, ensure BKT’s agent submits all the documents that are mentioned in the LC, with the desired contents. And if BofA is satisfied with the contents of the documents, it will release payment to SBI (for BKT).

But before that, let’s see what the steps in international trade under LC are, at a very high level.

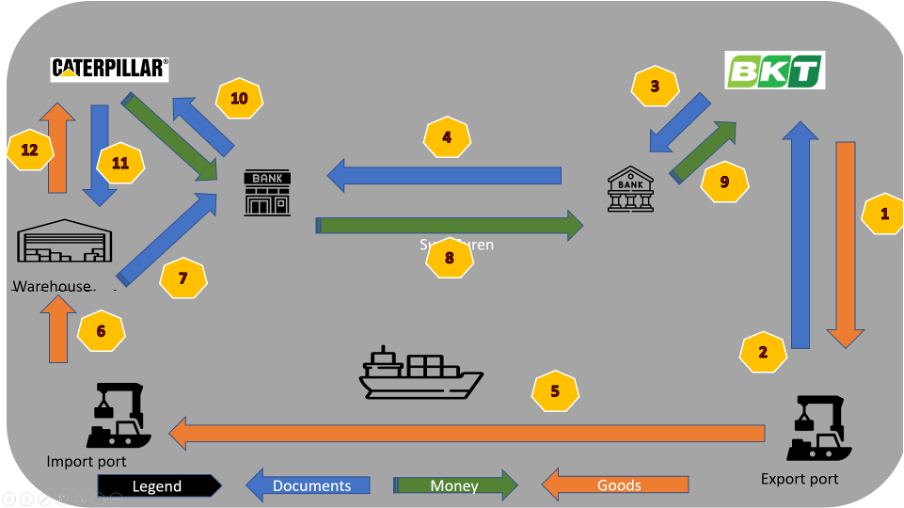

Consider the below picture, follow the numbers on the arrow for the sequence of steps. (This picture is AFTER both CAT & BKT have contracted with each other and BofA has also ISSUED the LC in BKT’s favour). In a sense the below is the actual flow of goods, documents and payments sequence. Arrows are colour coded.

Step 1: BKT sends the consignment of tyres to its freight forwarding agent, who will liaison with

(a) the export customs and get the necessary paperwork done,

(b) engage a shipping company that will take the tyres to Illinois, arrange to load them on to the ship.

(c) take out freight insurance.

Each of these entities will issue documents like export certificates, bill of lading, insurance policy etc.

Step 2: These documents are sent to BKT. The bill of lading is an important document that confirms that the shipping company has taken possession of the goods as described in the LC AND has loaded on to the ship headed towards where CAT wants.

Step 3: BKT hands over these documents to SBI, which verifies if these are as mentioned in the LC (if not, it will be iterated enough number of times to ensure they are as per the LC).

Step 4: SBI sends these documents to BofA to claim the payment.

Meanwhile, in parallel, the goods set sail to the destination port in Step 5: and are unloaded into the customs warehouse there (as in Step 6).

Step 7: All customs related procedures will be performed by CAT / its agent with the customs in the import country. Customs’ clearance & approvals are essential.

Step 8: Based on all documents (Bill of lading, Bills of exchange, Insurance, packing lists, certifications if any, etc.) that BofA has received, it takes a decision to accept or reject the payment and if accepted, they arrange to make payment to SBI as per the terms of the LC [could be immediate payment (called sight) or a deferred payment (usance)].

With this, two things happen.

(a) The transaction as per the LC is now complete from BKT / SBI point of view as their payment (or its assurance) is done. (Step 9)

(b) The title for the goods shipped are now transferred to CAT.

Step 10: All the documents that establish title to the goods and as required by the customs warehouse to release the possession of the goods are handed over by BofA to CAT, which can now share these documents to customs (Step 11) and receive the tyres (Step 12). Only at this stage CAT will get to lay its hands on the goods they purchased.

The payment terms between BofA and CAT are mutually agreed based on their relationship and upfront agreements. CAT can make the payment immediately to BofA or choose to convert the payment BofA made to SBI as a loan (much like ‘buy now pay later’), but this is between a customer and a banker as the international trade part is already complete.

BKT is happy that it received payment as long as it complied with the process and CAT is happy that payment was released only when its trusted banker verified all the documents are as per the LC conditions CAT jointly drafted.

Above is a simple flow and there are multivarious sub steps / complexities in each of the above steps. Our objective is not to get in deep but to have an overview of this process.

It is important to realise that all the communication between BofA, SBI and any banks in between are through the trusted network between banks — SWIFT.

Right from issuance of an LC to its lifecycle (issuance, additions, amendments, pre-advice, reporting discrepancies, acceptance or refusal, there are several types of messages under the MT700 series. MT stands for Message Type and each area is banking is covered by a series. 700 series (commonly written as MT 7xx) is dedicated for the LC type transactions.

Alongside, you would have also noticed (if not, please notice now), how a trusted messaging system is essential for the banking system to work and why it is important most banks in the world be part of it to move the wheels of the international trade machine.

We haven’t concluded yet as we are to see how the payment actually happens across borders. That, is a matter for our next article! See you soon.

Click on the urls below the images below to view the previous and next articles in this series

https://curiously.me/trust-trade-transact/

https://curiously.me/show-me-my-money/

Would you like to share this with someone you know? Please make use of the buttons below.

We saw how money helps in exchanging goods & services in this article. But what do our exporters do when they have to deal with buyers in countries that have their own money, issued by a different institution than ours, with a different guarantor than the one we trust.

Obviously the simplest way for an exporter is to quote a price in the currency of his home country. But it should be acceptable to the buyer (importer), for whom her home currency is different.

Why would a buyer or a seller hesitate to deal with currency which is not their home currency? Is it trust in a currency? Or is it a more practical consideration. There are two simple reasons which we will see below.

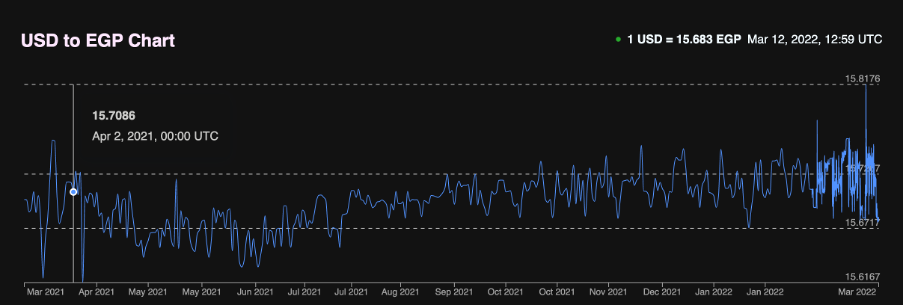

1. Stability: Imagine a carpet exporter in Turkey who prices a particular variety of carpet at 100 TRY (Turkish Lira) apiece when he sells within his own country. He would like to charge the same when he exports them too. As long as he quotes the price in TRY, there is no currency risk for him. But let’s assume the importer — who lives in Egypt- prefers not to pay in TRY and wants to pay only in EGP (Egyptian Pounds). Our exporter submits a quote in mid Dec 2021, where the exchange rate between the two currencies was 1 EGP = 1 TRY. So the carpets will be quoted at 100 EGP (which would have translated to 100 TRY). This looks simple. But we need to understand currencies can be volatile, (i.e the extent to which exchange rate varies on a given day is high). Below is a chart of exchange rate between EGP and TRY for the past one year. (Credit: xe.com)

One year exchange rate history between EGP and TRY. Credit:xe.com

Now, international trade doesn’t happen in an instant. Importers seek quotes from various exporters across countries, take their time to evaluate and then place the order. Suppose our importer in Egypt wants to place an order in mid-Jan 2022. The importer would be willing to pay only 100 EGP as that was the quoted price per carpet.

As we can see from the chart above, the exchange rate between EGP and TRY changed in Jan 2022 to 1EGP = 0.70 TRY when the deal is signed. Now if the payment were to happen immediately, our Turkish exporter would have got only 76 TRY for each of his carpets instead of 100 TRY, thereby incurring a loss if he goes ahead with the deal. All because the exchange rate was very volatile.

So just quoting the price for the order in a volatile currency is very difficult for the exporter (& to the importer if the opposite had happened). However if they were to agree to price the goods in a more stable currency, where the volatility is less, it brings some stability in the trade process. So exporters around the world want to quote the price of their goods in currencies that are less volatile. Let’s call this stable currency, XYZ for now.

2. Exchange rate risk. Let’s say our exporter “receives a confirmed order”. This means he has locked in his price in a (relatively) stable currency XYZ. This does not completely eliminate his price risk. International trade usually has a time lag between the time an order is placed and the final payment is made (more on the why in a later article) — say 3 months. There is every chance that the exchange rates between XYZ — TRY and XYZ — EGP changes in these 3 months. But this exchange rate risk can be mitigated by both the exporter and the importer by taking out currency forward contracts with their respective banks. The bank will charge a fee for this, but this mitigation gives certainty to both the importer (on how much she has to pay) and the exporter (on how much he will receive) in their respective local currencies.

A question can come in your mind, if exchange rate risk can be mitigated for a fee, why not do it at the time the quote was prepared, i.e in Dec 2021 itself? We need to remember, in Dec, there was no certainty that the importer will accept the order; so there is no cash flow expected to cover the risk. Whereas in Jan once the deal is signed, there is a contractual obligation for the importer to pay and certainty on a certain amount to be paid and received.

There will be volatility between any two currency pairs but the extent of volatility will be less if one of the currencies is a stable currency (XYZ).

Enough of talking in variables, what happens in real lives? What is the stable currency in which most trade happens in the real world? Most trade is quoted in USD (the reasons are long but the undeniable fact is, it is a currency backed by the US govt and trusted by almost the entire world to be relatively stable). A few other currencies also enjoy this trust, (EUR, GBP, JPY & CHF) but not to the extent of USD.

Lets see how the two currencies performed w.r.t USD. Below are one year historical charts of exchange rates.

First between USD and TRY. Credit: xe.com

One year exchange rate history between USD and TRY. Source: xe.com

The chart looks almost similar to the EGP TRY chart, indicating that it was TRY which had had a volatile year.

Now, if we see the exchange rate between USD and EGP in the same period, it looks like this. Credit: xe.com

One year exchange rate history between USD and EGP. Source: xe.com

The chart looks volatile but within a very narrow band. So most of the exchange rate volatility between EGP — TRY was due to high volatility of TRY and moderate volatility of EGP.

3. Fungiblity of the trade currency. While all money is fungible in theory, it has boundaries. Real fungibility happens only when the earned currency can be ‘used’ to purchase any other goods / services from a different country. Assume that our exporter quotes his goods in EGP to his Egyptian client and also receives EGP upon sale. He will now have EGP funds with him. Unless he has to buy something quoted in EGP (most likely from Egypt), he has to convert his EGP into a third currency. Take for instance that he needs to buy weaving machines from a vendor in Germany, his EGP will be of no use and he has to convert EGP to EUR which involves transaction costs and fees to bank (even if we ignore currency volatility for a moment). So exporters and importers, prefer to have a single currency that is acceptable by traders across borders.

4. Government diktat. Yes, as part of managing the economy, governments also dictate — for good reason- what currencies their international traders can deal in. This is because, governments, primarily through their central banks maintain what is called “Foreign currency reserves”, to ensure they have adequate currency to pay for their countries’ imports. Central banks cannot be holding (& maintaining) a balance in several currencies like EGP, TRY and may prefer to hold only in certain currencies (like USD, EUR, JPY etc.) that are not very volatile. (None of us would want to hold an asset ( a reserve) whose value is volatile isn’t it). Due to this, any importer or exporter of a particular country are allowed by their governments to trade in only a few currencies. Purists might want me to tell you about the gold standard, the Bretton Woods agreement of 1944, and more importantly its undoing in 1971 for why the USD is a preferred trade & reserve currency worldwide. They are correct. But we will keep it for a later day. If you are interested, you can check that out along with the concept of petrodollars. Right now I want to cover the more basic reasons as to why a stable currency is needed for trade.

Now when you zoom out and find a list of commonly preferred / allowed currencies across countries, it is a very small list and the most favoured currency is just one. And that is why, most international trade is quoted in USD.

Click on the urls below the images below to view the previous and next articles in this series

I can imagine you chuckle at this question, but I ask you why do we need the “concept” of money? Let’s understand this first at a beginner’s level. I hope to progressively expand this for a more deeper understanding later, but for now, the basics.

Money is a financial tool, an invention nearly as old as agriculture and wheel.

But present day ‘Money’ is also a story. Before we get to it, let’s see what happens if the concept of money did not exist.

We all have needs & wants, but we cannot produce all that we need and create all that we want. Some examples of the limitations are:

– My location doesn’t help (I cannot grow apples in my geography or have petroleum beneath my ground).

– I don’t have the know-how to produce it (from growing vegetables to making automobiles or aircraft).

– I may not have the authority to do it (build a copper smelting plant or start an iron foundry in my garden).

– Social contracts may prohibit (I cannot bury my dead in my apartment compound).

Since we cannot produce everything we need, there is a necessity to trade, exchange goods & services — even for personal needs (food, transportation, haircut, tuitions etc.)

Barter was an option that was very popular at one time (and even used very occasionally in this day and age) but it is not convenient. For those who aren’t familiar with barter, this is how it goes.

– I have something that I am ready to give away in exchange.

– Another person has something I want.

– The other person should have a need (or a want) for the goods I have — at the same time I need what the other person has. (‘coincidence of wants’).

– We both are accessible to each other (or we would need some intermediation service like that of a broker)

– We both are acceptable to exchange with each other.

– We need to establish the value of each others’ goods (how much gold for a haircut or a glass of milk) in each trade. This also means we need to publish the price list of all commodities in every other commodity / service. This discovering the price of each item against another can be daunting, and even unfair at times.

– Minimum transaction quantity became a problem (cannot give half a haircut for a litre of milk)

– Physical exchange has to happen.

Since there were so many limitations, we needed to have an intermediary medium of exchange that had certain characteristics.

It should have value — not necessarily in itself but should be able to buy value at will.

Should be convenient to use, store, retrieve, transfer the title. I own 100 US dollars and if I give it to you in cash or deposit in your account, it becomes yours.

Fungible (a 1 dollar coin and a 1 dollar note have the same value — even though the material (intrinsic) value for both are different). Similarly 100 cents and 1 dollar are the same value, irrespective of the shape and form.

It should be durable. Not only should it be available across time but also weather any wear & tear. Let me explain. I stash cash under my mattress, forget about it and be able to use it after a year. Also my one dollar note is torn? I should be able to exchange it for a new one dollar note.

Establish “Price” for every good or service with a single rate card. For example, 10 dollars for a haircut, 5 dollars for a litre of milk or a Kg of Rice. As opposed to 2 litres of milk or 2 Kgs of rice for a haircut or half a haircut for a litre of milk.

But the most important characteristic of all is the acceptance. Others in your community should “accept” that it is currency. Pokemon cards and Monopoly money too are currencies — but with limited acceptance within a closed group. But a true currency should be acceptable across a wider community of people — usually across a country or a wider region.

So came the tool called money as a medium of exchange.

What forms of money have we seen?

Cattle

Precious or semi-precious stones

Precious or semi-precious metals. Gold, Silver, Iron, Tin, Copper, Aluminum, Nickel (rings a bell isnt it)

Salt….(the etymological root to the word Salary)

Each of the above served as money for a while in its time. And they also had their limitations, so a new virtual value was created — Printed or Minted money — with a guarantee by the issuing authority — a king or a central bank in today’s world. Of course, for keeping the trust on the guarantor, the country has to have a robust economy, a mighty power – both military power & soft power – to make sure that guarantee is believable.

Today, central banks issue a guarantee on a piece of paper or cloth (that costs say 50 cents) and call it — say 10 dollars. Although the physical piece of paper costs only a few cents to make, we are ready to believe (in the story) that it is indeed 10 dollars because of the guarantee. That is how a guarantee became currency.

Money underwent a A BIG TRANSFORMATION. We settled for and accepted an apparently value-less (or less value than indicated) commodity due to the trust we have in the guarantee & the guarantor.

The biggest factor for a currency’s success is when both the buyer and seller TRUST that a fair value exchange has happened, even when one of the commodities is just a piece of paper.

Over the last couple of decades, with modern technology in banking, we don’t even exchange paper anymore but are satisfied with a virtual electronic unit.

The most popular form of ‘present day’ money is a magnetic medium, that holds an electric charge in the form of binary value, stored in some remote location inaccessible to the general public. We don’t hold it in our hands, we don’t even see it, but are happy with a bank statement, an email or even an SMS, that says we have money in our account. That is the story called money that most of us believe in.

Picture Credits

Collage made from pictures, thanks to: Steve Ruby & Shubham Dhage on Unsplash and gorartser & LeonMay on Pixabay

Click on the urls below the images below to view the previous and next articles in this series

Cursory google searches would have told you what SWIFT (Society for Worldwide Interbank Financial Telecommunication) is. I am not going to repeat it but will help you relate to it and tell you why it is important, briefly.

SWIFT Logo for representation purposes. Copyright with SWIFT

SWIFT is a messaging system. Yes, it is like email for banks. Only banks around the world can send and receive messages between themselves in this messaging system. And it has to be about a financial transaction. Which means they cannot exchange cute cat videos or talk about weather. Banks generally use SWIFT for asking for payment, instructing one another to make a payment, send each other confirmations of treasury or trade transactions they did amongst each other. Each message is an instruction or an important FYI that results in a financial action on the other side.

So why the big fuss if it is like an email system between banks. Open your email inbox now, yes now! See for yourself the loads of messages sitting in your inbox, junk box and spam box. Deep inside you will also see a mail from a Nigerian Prince wanting your help (payment request) to send you loads of money (Payment instruction). Smartly you ignored the message which could have otherwise costed you money and acidity.

To avoid the pesky Prince and other fraudsters, SWIFT has an elaborate system of authenticating senders and receivers of messages, which ensures that all message senders are authenticated (the banking version of a Twitter blue tick). Many of them have an added layer of identification between themselves through bilateral (key exchange) mechanisms. As a result, if a bank receives a SWIFT message, it is authentic, received from who they claim themselves to be and the message is ‘actionable’ . There are additional acccount mechanisms, but for the purposes of our understanding, suffice to say, it is a very authentic messaging system that keeps ALL SPAM out.

Reliable & Secure: “I haven’t received the email yet”. Some of us have used this excuse or know someone who has. Such excuses don’t work with SWIFT. In its 47 years of existence, SWIFT (claims that it) hasn’t lost a single message out of the billions that were exchanged in its platform. So secure is the platform that if a bank says they sent, the recipient bank would have received it.

Not only has SWIFT not lost a single message, but the platform is so secure that no one else was able to hack or gain access to messages that were not meant for them. Yes I hear that you have heard about hacks (Bangladesh central bank etc.) but these were login credentials abused instead of the SWIFT platform yielding to hackers. Again, not a single hack in almost half a century!

Some feat!

Automation: These days we live in an API driven world where our email talks to our bank, one application talks to another etc. But SWIFT has implemented automation (which it calls ‘Straight Through Processing’) for the last 20+ years. To facilitate this, SWIFT has standards and rules on how messages are to be structured, how each field needs to be filled for each business case and so forth. So, a huge portion of the millions of messages exchanged everyday have not seen human hands at all. They all have been generated by, handed off to, received by, read and acted upon automatically , by the myriad software applications in a bank [Core banking applications, Payment (product) Processors, Payment hubs, message queues and other technical jargons your friendly neighbourhood tech guy might help elaborate].

What is the big deal you may ask, RPA is a thing and a pilot too puts his plane on autopilot. Just like how the autopilot reduces human errors and saves lives, automation in SWIFT message processing reduces errors (financial — yeah your money), speeds up transactions (in most cases less than a day but not more than two) and thereby reduces cost for you as a customer of a bank.

Standard, widely used. We know countries can’t agree on political systems, can’t agree on borders between them and proudly agree to disagree on several areas. But if there has to be a stellar example of worldwide agreement on something that has held for a long time, it is the standards published by SWIFT. So in a sense, it is truly one of the very few things the world agrees on — before expelling some specified banks due to politics that is.

There is much much more to SWIFT than this article, but for someone who wants to understand what the big fuss is about, I believe this is a good starting point. Let me know your thoughts.

Would you like to share this with someone you know? Please make use of the buttons below.